The Big Picture |

- The scarcity value of Treasury collateral

- High Quality Liquid Assets and Munis

- 10 Monday PM Reads

- Ray Dalio & Larry Summers Discuss How the Economic Machine Works

- Corporate Deadbeats (Newsweek Cover)

- Changes in U.S. Family Finances from 2010 to 2013: Evidence from the Survey of Consumer Finances

- Demand for Financial Advice Isn’t Going Away

- 10 Monday AM Reads

- What Is Alibaba?

- When and how should the Fed exit?

| The scarcity value of Treasury collateral Posted: 09 Sep 2014 02:00 AM PDT

|

| High Quality Liquid Assets and Munis Posted: 08 Sep 2014 04:30 PM PDT HQLA and Munis

High Quality Liquid Assets (HQLA) is a term that now applies to the implementation of the Liquidity Coverage Ratio (LCR) in the Basel III Rule. This highly technical mouthful of acronyms and rules specifically applies to banks, their liquidity requirements and the rules governing the securities in their investment portfolios. The targets of the new rules are the big banks. According to an analysis by BMO Capital Markets, "In general it will require banks with more than $250 billion in assets to hold enough HQLA to cover 100% of a projected 30-day cash outflow in a stressed scenario." BMO notes that banks holding over $50 billion will have to meet a "lighter version" of the requirements than will banks with over $250 billion. Small banks with under $50 billion are in a different category and are not considered by regulators to be systemically risky institutions, so the new rules do not apply to them. What does all this have to do with municipal bonds? The HQLA rules as defined by the Federal Reserve (Fed) for US banks have excluded municipal bonds from this category of securities that must meet the LCR. Corporate bonds, certain equities, conventional mortgages, federal agency securities, and U.S. and other OECD sovereign debt are included. Multiple issues arise for investors in the wake of the new rules, though readers must note that this is a fluid rulemaking determination and things may change. We will address some issues as we see them in this current and evolving regulatory structure. It is important to note that investment-grade corporate bonds have a default rate that is 36 times higher than the default rate on investment-grade municipal bonds. This determination is based on information from Moody's and compiled on investment-grade defaults from 1970 to 2013. In other words, the Fed has defined into the rule those corporate securities that have 36 times the default rate, historically speaking, of investment-grade municipal bonds that the Fed has excluded from the rule. To give an example: the bond of Johnson & Johnson, a corporation headquartered at Exit 9 of the NJ turnpike is included, but NJ Turnpike Authority debt is not. Both bonds are quite liquid and easily traded, and both are high-grade ratings. Why the Fed made this decision, which would include JNJ and exclude NJ-TPKE, is still not completely clear. There is discussion underway among market professionals who are attempting to get the Fed to change its view. What the rule means for municipal bonds is that a support mechanism in the marketplace that would have facilitated the issuance of municipal debt is weakened by a new rule. As a result, it will cost municipal bond issuers more to achieve their financing. There are various estimates of how much more it will cost – these issuers are all guessing. The fact is that it will take time to determine exactly how banks will hold municipal debt in the future, after the market has adjusted the price or yield to make up for the difference made by the rule. There is an area in which municipal bonds will be surely impacted. That is in the "bank-qualified" smaller issues. BQ was an exception made in the Tax Reform Act of 1986 to facilitate the issuance of municipal debt by smaller issuers. Those bonds are not highly liquid and it would have made sense for the Fed to exclude them in a liquidity calculation. In most cases, the banks holding BQ debt are servicing local customers that are municipal entities and assisting them with financing. That is why the Tax Reform Act of 1986 provided special incentives for banks. We now have a situation resulting from a change in a tax-law incentive that had been in place for decades. The Fed has issued a rule that has offset or reduced that incentive. A tension between incentive and disincentive is at work in the small-bank qualified-issuer municipal bond market. In the United States, a large number of the 90,000 municipal bond issuers fall into in this BQ category. Their cost of financing will certainly rise by some amount. Let's get to what the new HQLA rules mean for investors. In one way, this is good news. We are taking bond buyers (large banks, for instance) who traditionally participated in parts of a bond market, and removing some of those buyers or imposing a new cost on them. The impact raises tax-free yields to offset the change. Individual municipal bond investors will like this new rule because it results in a higher tax-free interest rate for them. There is more prospective tax-free income for owning municipal bonds. As attractive as municipal bonds may have been in the past, they will be even more attractive because a competing buyer (the larger banks) is being removed or reduced. How this ultimately plays out in a $3.7 trillion US municipal bond market remains to be seen. We know the rule currently impacts municipal bond issuers in a negative way. At the present time, there is no indication that the rule is going to be changed. In the US, at intermediate and long maturities, the tax arbitrage available in the income tax code for tax-free bonds is minimally applicable. Market forces are pricing municipal bonds of long maturities at relative bargain rates. We see that today when we compare a long-term, true-AAA, highest-grade, tax-free bond with an equivalent long-term US Treasury taxable obligation. When we do that, we find the interest rate paid on those tax-free bonds in current market conditions is approximately the same as that paid on the taxable bond. In other words, market agents and forces are pricing the municipal bonds as if there is no income-tax code. That makes no sense. We also know that when we get to the shorter-maturity end of the yield curve, we see the yield on tax-free way below the taxable yield. In the shorter end the tax arbitrage is almost fully applied. In the middle of the yield curve, the tax arbitrage of the US income tax code is somewhat fully applied, while at the longest maturities it is virtually nonexistent in market pricing. So, as one goes from shorter to longer maturity, the tax arbitrage component diminishes. We think HQLA will only exacerbate this anomaly. The bottom line of HQLA is that a change has occurred that will alter market-pricing references by some amount. We do not know how much. HQLA rules will benefit the individual investor who selectively manages municipal bonds and chooses them skillfully. The individual investor will gain at the expense of the large banks, which will be adversely affected to some degree. Small banks are not affected. The details will be revealed as markets adjust to this new paradigm. Meanwhile, there are still relative bargains in the tax-free bond space. Investors who worry about rising rates can use hedging devices to dampen the volatility they would experience if and when rates eventually rise. David R. Kotok, Chairman and Chief Investment Officer |

| Posted: 08 Sep 2014 02:30 PM PDT My afternoon train reads:

What are you reading?

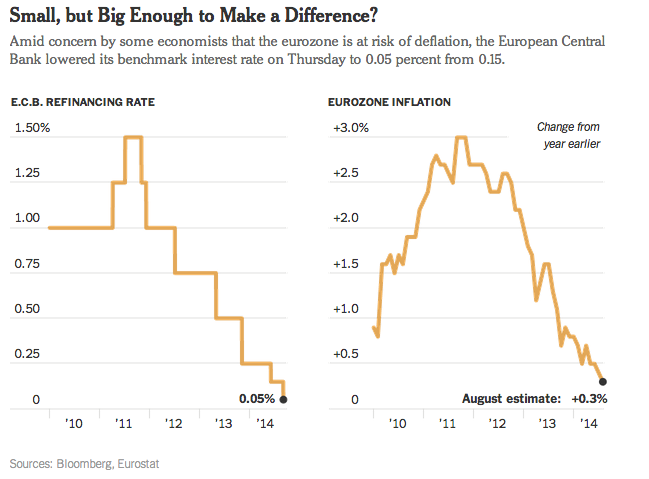

Europe’s Bank Takes Aggressive Steps |

| Ray Dalio & Larry Summers Discuss How the Economic Machine Works Posted: 08 Sep 2014 01:00 PM PDT The following conversation took place at Harvard University. Former U.S. Treasury Secretary, Larry Summers invited Ray Dalio, founder and chairman of Bridgewater Associates, the world's largest hedge fund, to discuss Dalio's unique views on economics. The conversation is based off of Dalio's 30-minute animated video entitled "How the Economic Machine Works" which is available on YouTube and at EconomicPrinciples.org. Larry Summers and Ray Dalio on Dalio’s Unique Perspective of “How the Economic Machine Works” |

| Corporate Deadbeats (Newsweek Cover) Posted: 08 Sep 2014 10:30 AM PDT Nice cover:

Source: Corporate Deadbeats: How Companies Get Rich Off Of Taxes, David Cay Johnston, Newsweek, September 4, 2014

|

| Changes in U.S. Family Finances from 2010 to 2013: Evidence from the Survey of Consumer Finances Posted: 08 Sep 2014 09:30 AM PDT |

| Demand for Financial Advice Isn’t Going Away Posted: 08 Sep 2014 06:00 AM PDT |

| Posted: 08 Sep 2014 05:00 AM PDT This is the week the year starts in earnest: 5 full days of work, kids at school, no one on vacation. Start your day with the most important meal of the day, your AM reads, fortified with riboflavin:

|

| Posted: 08 Sep 2014 03:00 AM PDT Alibaba, China's largest e-commerce company, is preparing to go public in New York, setting up expectations for the biggest stock market debut in United States history. |

| When and how should the Fed exit? Posted: 08 Sep 2014 02:30 AM PDT

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment