The Big Picture |

- Tight Credit Conditions Continue to Constrain the Housing Recovery

- 10 Monday PM Reads

- Masters in Business: Now on iTunes!

- Mark Cuban’s Dozen Rules for Startups

- Zombie Ideas? Blame the Billionaires…

- 10 Monday AM Reads

- Athena – Goddess of War on the Close

- A Tale of Two Economies — It Was the Better of Times, It Was the Worst of Times

| Tight Credit Conditions Continue to Constrain the Housing Recovery Posted: 21 Oct 2014 02:00 AM PDT |

| Posted: 20 Oct 2014 01:30 PM PDT My afternoon train reads:

What are you reading?

Natural-Gas Prices Fall Even With Chill Nearing |

| Masters in Business: Now on iTunes! Posted: 20 Oct 2014 11:00 AM PDT Finally, the long awaited appearance our series Masters in Business is now on Apple iTunes! All of our prior interviews are here, as well as all of the podcasts extras. And, all of our future guest interviews will show up here as well! Click to subscribe!

|

| Mark Cuban’s Dozen Rules for Startups Posted: 20 Oct 2014 09:45 AM PDT I found this today while researching materials for a related project, and I thought it was pretty interesting:

|

| Zombie Ideas? Blame the Billionaires… Posted: 20 Oct 2014 08:00 AM PDT

I began my career in finance on a trading desk. You learn some things very early on in that sort of situation. One of the most important things is that while it’s OK to be wrong, it can be fatal to stay wrong. Unfortunately, that standard doesn’t apply to people whose work isn’t evaluated on a daily and objective basis via their profit and loss results. In many fields, such as politics and policy-making, there are lots of shades of gray when it comes to being right or wrong. And quite bluntly, that is a shame. As a society and a nation, we would all be better off if the people who are consistently wrong paid some sort of price for those errors. Unfortunately, that doesn’t happen enough these days. Some bad policy decisions will lead to the occasional elected official being turned out of office. That — unfortunately — is the exception, not the rule. I doubt history will rank George W. Bush and Barack Obama among our great presidents , but both were re-elected despite being unpopular. Between gerrymandered congressional districts and apathetic voters, even the most incompetent elected official has almost lifetime tenure. What underlies all of this nonrecourse bad policy? It is much more than corporate lobbying and partisan politics. The worst of today's political malfeasance is being driven by failed ideologies. Zombie ideas that refuse to die have become enshrined in our collective intellectual legacy. The people behind these have been insulated from the economic costs they impose. Blame the billionaires.

|

| Posted: 20 Oct 2014 05:00 AM PDT In case you missed it, yesterday was the 27th anniversary of 1987 crash – in 2014 terms, that would be a one day drop of 3700 Dow point! Oh, and reads:

|

| Athena – Goddess of War on the Close Posted: 20 Oct 2014 04:00 AM PDT Themis Trading commentary Athena – Goddess of War on the Close

Do you, as fund managers and traders, trade The Close? Do you target The Close? Do you trade in the last 10 minutes of the day? If so, then this morning note is for you. While Modern Markets has lately been quite active defending high frequency trading by orchestrating television appearances for Bart Chilton, and puff pieces in the WSJ about Hudson River Trading, the SEC has been quite busy. Yesterday it announced its first ever action against a high frequency trading firm for market manipulation – and manipulating the most important prices in the equity markets – the Closing Price. While the SEC brought this case against Athena Capital Research LLC (not to be confused with Athena Capital Advisors), it did so without Athena executives admitting nor denying any wrongdoing, and it did so without naming the executives. Who are those executives? Our efforts to find out who they are have only turned up a few possibilities. For example there is a reference to a BATS board member in this article that references a Mr. Peter Buckley, of Athena Capital Research LLC: Tradebot is "incredibly successful," said Peter Buckley, COO of New York-based Athena Capital Research LLC. "Their growth is a direct result of Dave's vision, of his ability in hiring superior talent — that's sort of step one," said Buckley, who met Cummings while serving on the BATS board. "The next step is guiding the talent, keeping them competitive, keeping them on point and working together toward one goal." This Peter Buckley is also on one of the CFTC's sub-committees on HFT !

What did Athena actually do? Athena systematically and algorithmically manipulated the NASDAQ auction Closing Price in thousands of securities throughout 2009 at the very least. They had HFT programs called "Meat" and "Gravy" specifically designed to manipulate the closing price. Their algorithms read the NADSAQ imbalance information blasts, and reacted in intentionally nefarious ways. The SEC gives a lot of detail on some of the specifics, including examples of what Athena did in EBAY. Please look at the SEC filing that we linked to; it lays out the blow by blow in an amazingly easy-to-understand way. Anyway, here are just a few excerpts: Athena referred to its accumulation immediately after the first Imbalance Message as "Meat," and to its last second trading strategies as "Gravy." In early 2009, Manager 2 described this pattern in an internal Athena email as follows: "We have a desired accumulation pattern which includes grabbing stock at the beginning, a period of 'average price' accumulation, and a crescendo at the end." As a result of these steps, during the Relevant Period, Athena's Imbalance-Only Orders were filled at least partially over 98% of the time and the firm traded on the entire imbalance of almost every imbalance it wanted. Athena referred to this in internal emails as "dominating the auction" and "owning the game." And here are some quotes taken from Athena managers, owners, partners and officers of the firm: - "Let's make sure we don't kill the golden goose." - "We can have some aggressive gravy if we know we have a 100% chance of getting the fill." - "Biggest dollar move" … "percentage move" … "Looks like we have some Mach chips….going to Vegas tonight…." - "To make sure we always do our gravy with enough size." - "The lack of the blast resulted in extremely poor prices (we essentially gave someone else all the liquidity they wanted with no price impact at all)."

The last email quote is particularly sad – Athena laments that they did now screw the buyside managers targeting the close as well as they wanted to.

Is this SEC Athena case a Big Deal?

The Closing Price is not just any price. Of all the thousands of price points throughout the trading day, it is the most important price. It is used to price mutual funds and ETFs. It is targeted in trading strategies by the buyside (Target-the-Close algos, VWAP algos, etc.) While many in the media are proclaiming this a small case (SEC Brings small, but Important Case against HFT), it actually is not.

Regulators, including the SEC, have always been especially harsh in their view of those who manipulate closing prices. The CFTC took action against HFT firm DRW Investments for this activity. The SEC has also been somewhat harsh when encountering it in the past:

- In 2002 the SEC fined Piper $100K because one employee helped one customer mark the close in one stock. - In 2003 the SEC fined SLKC $450K because employees helped one customer mark the close in one stock.

In the Athena case, we have several employees manipulating, not one stock, but thousands. Not on one day, but every day. The Athena managers, officers, and employees wrote code to accomplish this, and did so brazenly. They wrote about it in emails. They were deliberately manipulative even to the point where they debated internally whether they would get caught, and asked themselves if they were risking "killing the golden goose."

We Have Five Questions:

1) This Athena activity is from five years ago. Five. Why did it take five years to fine them and bring this action? 2) Who cleared Athena's trades? If it was one of those HFT sponsored-access type firms, like Newedge, did they not monitor their customer's trading for fraud? 3) Are there other small "rogue-ish" firms like Athena, also using sponsored pipes, who have engaged in this activity? If I were a regulator, and knew that Athena cleared though and used the pipes of Acme Sponsored Access Firm, I would want to see their client list, and look at each of their clients' trading activity closely. 4) We presume NASDAQ, who had no comment on this case, watches for this activity, and perhaps brought it to the attention of the regulators. We hope so. Do they monitor more aggressively for this today?

The most important question we have, however, is why did the SEC settle for a measly $1 million fine with a "neither admit nor deny", and keep the perps' names out of the filing? (If they could fine $450,000 for marking the close in just one stock, how can they justify only $1 million for Athena? Why the secrecy on who was involved? Summarizing:

All HFTs are not the same. Heck, we are not even sure what HFT means anymore. Clearly though, Virtu is not Tower (Latour). IMC is not Panther. KCG is not Jump Trading. Citadel is not DRW. And none of those firms are Athena. Some firms are clean, transparent, and valuable to the marketplace – they make markets, and do so without strategies designed to detect and disadvantage investors. And in the process the may even make substantial amounts of money – that's more than ok with us. Some firms, however, engage in manipulation and deceit, and are a black eye on our industry. They need to be caught and fined hard, and maybe even banned from the industry. If the SEC were thusly harsh, a message would be sent to the investing public that the SEC takes their needs seriously, and it would greatly enhance confidence in the marketplace. Right now, after reading the SEC- Athena action, we feel no such confidence. We can't help but wonder how many additional small firms are just like Athena. We feel that a $1 million fine with a "neither admit nor deny" is a joke and an insult. We can't wait for the next lobbyist-sponsored puff-piece in the major media. That will make us feel better. - See more at: http://blog.themistrading.com/athena-goddess-of-war-on-the-close/#sthash.4DRILWOp.dpuf |

| A Tale of Two Economies — It Was the Better of Times, It Was the Worst of Times Posted: 20 Oct 2014 02:30 AM PDT A Tale of Two Economies — It Was the Better of Times, It Was the Worst of Times

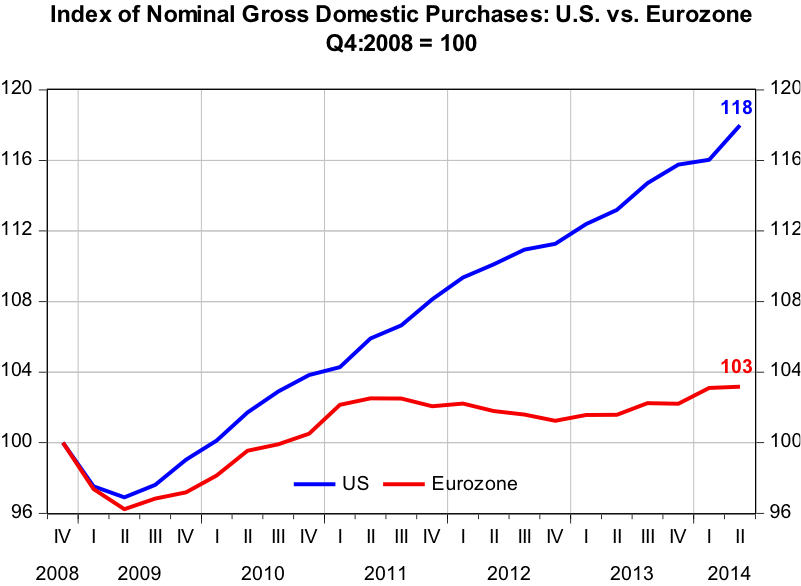

A Tale of Two Economies – It Was the Better of Times, It Was the Worst of Times As quantitative easing comes to an end (apparently) by the Fed and is taken up by the European Central Bank (ECB), let's compare the behavior of nominal domestic demand in each central bank's economy and venture a reason for any differences. Plotted in Chart 1 are index values of the nominal Gross Domestic Purchases in the U.S. and the eurozone, respectively. Each index is set at a value of 100 for Q4:2008. Since Q4:2008, Gross Domestic Purchases in the U.S. increased a net 18% through Q2:2014 (that is what the index value of 118 indicates). For the eurozone, Gross Domestic Purchases increased a net of only 3% in this same time period. In terms of compound annual growth rates over this period, the U.S. experienced growth of 3.0% and the eurozone, just 0.5%. Chart 1

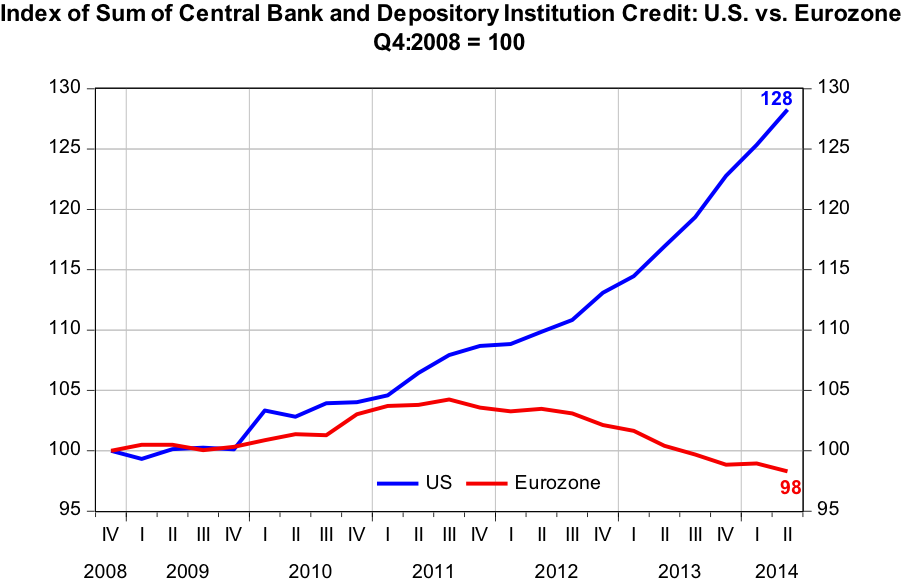

Now, let's examine the behavior of credit created by the central banks and depository institutions in each of these economies. This is credit that is created figuratively out of thin air. When central banks purchase securities in the open market, such as they do when they engage in quantitative easing (QE), they create credit out of thin air. When the depository institution system expands its loan and securities portfolios, it creates credit out of thin air. Credit created out of thin air enables the borrower to increase his/her current nominal spending while not requiring any other entity to reduce its current spending. Plotted in Chart 2 are index values of the sum of central bank and depository institution credit outstanding for the U.S. and the eurozone, respectively. Each index is set at a value of 100 for Q4:2008. Since Q4:2008, U.S. thin-air credit increased a net 28% through Q2:2014, which works out to be a 4.6% compound annual rate. In this same period, eurozone thin-air credit has contracted a net 2%, or at a compound annual rate of minus 0.4%.

Chart 2

The Fed has engaged in QE in three separate phases in recent years, the first of which commenced in Q1:2009. From the end of Q4:2008 through the end of Q2:2014, U.S. thin-air credit increased a net $3.692 trillion, 82% of which was contributed by the Fed. During this same time period, the compound annual rate of growth in depository institution thin-air credit was only 1% rounded. Recall, that the sum of Fed and depository institution thin-air credit grew at a compound annual rate of 4.6% during this 22-quarter period vs. a long-run median annual growth rate of 7.4%. During this period, the ECB has refrained from engaging in QE and eurozone thin-air credit has contracted on net. Had the Fed not engaged in QE, U.S. total thin-air credit growth would have been quite weak, similar to what the eurozone has experienced.

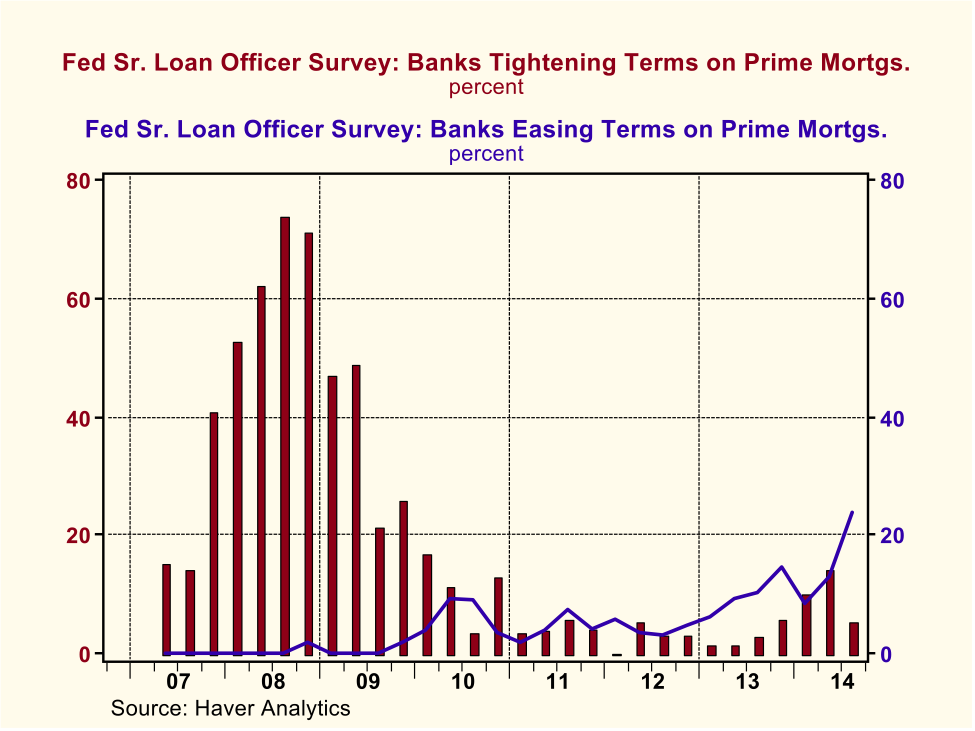

A clue as to why depository institution thin-air credit creation has been weak in both the U.S. and the eurozone can be found in former Fed Chairman Bernanke's recent revelation that he was unable to refinance his home mortgage. The explanation for weak depository institution thin-air credit creation is not so much related to lack of demand for it, but rather depository institutions' inability to supply demanded credit. Following the bursting of the residential real estate bubbles in the U.S. and the eurozone, depository institutions experienced a severe "evaporation" of capital. Because of capital constraints, depository institutions were not able to expand their holdings of loans and securities. In the U.S., depository institutions relatively quickly began repairing their capital deficiencies. At the same time, however, regulators increased capital requirements and imposed more stringent liquidity and other regulatory requirements on depository institutions. Thus, while someone with a relatively high, but variable income, similar to Ben Bernanke's current financial situation, would have had no difficulty in qualifying for a mortgage in 2001, he now has greater difficulty. If Ben Bernanke had looked at some of the Fed survey data when he was Fed chairman, he would not have been surprised that he might have difficulty refinancing his mortgage once he became a "free agent". Plotted in Chart 3 are the responses to the Fed's quarterly Senior Loan Officer Survey of bank lending terms related to residential prime mortgage applications. As the housing bubble began deflating in late 2007, the percentage of banks tightening their prime mortgage terms began rising, skyrocketing in 2008. Although the percentage of banks tightening their mortgage lending terms tailed off significantly by 2010, the percentage actually beginning to ease their lending terms has only begun to meaningfully rise in 2014. Chart 3

The Fed conducts another quarterly survey that relates to banks' willingness to lend, the Survey of Terms of Business Lending. Plotted in Chart 4 are the survey results showing the average rate charged by banks in the survey on all commercial and industrial (business) loans minus the Fed's target federal funds rate. From Q3:1986 through Q4:2007, the median loan spread was 1.99 percentage points. The median spread from Q1:2008 through Q3:2014 rose to 3.05 percentage points, with the spread in Q3:2014 being 2.61 percentage points. These higher spreads following the financial crisis indicate banks' inability to supply demanded credit because of capital constraints and/or increased regulatory scrutiny.

Chart 4

In case you hadn't noticed, I have been attempting to make the case that the Fed's engagement in QE and the ECB's lack of QE account for the difference in the performance of the U.S. economy vs. the eurozone economy since 2008. But for all you Keynesians out there, what about federal fiscal policy, in particular federal spending? Some Keynesians (Krugman?) make the argument that the fiscal austerity in the eurozone is what has held back aggregate eurozone economic activity. Contrary to what some op-ed writers in The Wall Street Journal (Wesbury?) might have you believe, there has been fiscal austerity in the eurozone. In the five years ended 2013, the latest complete data I have, eurozone central government nominal spending grew at a compound annual rate of just 1.5%. And again, despite what some other op-ed writers in The Wall Street Journal (editorial board?) might have you believe, there also has been fiscal austerity in the U.S. To wit, in the six fiscal years ended 2014, total federal government nominal spending grew at a compound annual rate of 2.7% compared to a median annual change of 5.5% from FY 1981 through FY 2008. Total U.S. federal government expenditures in FY 2014 were actually $13.5 billion below those of FY 2009! Admittedly, federal government expenditures did soar in FY 2009 vs. FY 2008 because of TARP, the American Recovery and Reinvestment Act of 2009 (Obama's fiscal stimulus) and "automatic stabilizers" such as unemployment insurance and food stamps. The point is that in both the U.S. and the eurozone, there has been fiscal austerity in recent years. Yet, U.S. aggregate domestic demand has been considerably stronger than that of the eurozone. The tale of the two economies is that in one, the U.S., the Fed pursued a QE policy, resulting in the better of times. In the other, the eurozone, the ECB eschewed a QE policy, resulting in the worst of times.

Paul L. Kasriel |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

0 comments:

Post a Comment