The Big Picture |

- Yellen: Central Banking: The Way Forward?

- 10 Monday PM Reads

- Offshore Profits Avoid IRS Reach

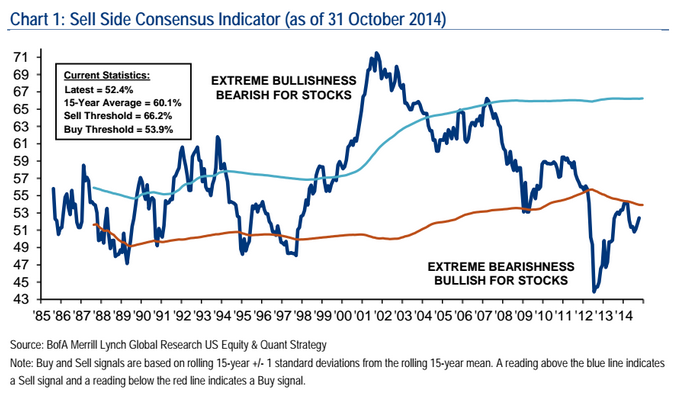

- Sell Side Consensus Indicator

- Apparently, You CAN Buy (Some) Happiness

- 10 Monday AM Reads

| Yellen: Central Banking: The Way Forward? Posted: 11 Nov 2014 02:00 AM PST At the “Central Banking: The Way Forward?”, International Symposium of the Remarks at the Panel Discussion on “Shaping the Future of the Macroeconomic Policy Mix”

Remarks at the Panel Discussion on “Shaping the Future of the Macroeconomic Policy Mix” I would like to thank the Banque de France for inviting me to take part in what I expect will be a lively discussion. The suddenness and severity of the global financial crisis forced policymakers to respond rapidly and creatively, employing a wide range of macroeconomic tools–including both monetary and fiscal policies–to arrest a steep economic downturn and restart the global economy. Given the slow and unsteady nature of the recovery, supportive policy remains necessary. Today I would like to briefly review the evolution of monetary and fiscal policies following the global financial crisis both in the United States and in other advanced economies, since we have faced similar experiences and employed similar policy responses. I will try to draw some lessons and provide some thoughts on the policy mix going forward. Policy before the Crisis Fiscal deficits also appeared to be under control before the crisis. According to the Organisation for Economic Co-operation and Development (OECD), general government deficits in 2007 were less than 4 percent of GDP in the United States and the United Kingdom, about 2 percent in Japan, and less than 1 percent, on average, in the euro area. Still, given relatively buoyant economic conditions, governments probably should have been doing more to prepare for the long-term challenge of aging populations, which will boost pension obligations and health-care expenditures in coming years. Moreover, government debt levels were already high in Japan and in some European economies and not particularly low elsewhere. In addition, some euro-area countries that appeared to have strong fiscal positions going into the crisis depended partly on revenue from housing booms that soon went bust. The Policy Response to the Crisis Initially, fiscal policy also provided significant stimulus. A portion of this stimulus reflected the operation of automatic stabilizers–higher unemployment benefits, for example, and a decline in tax payments due to lower incomes–and some came through cuts in tax rates and increases in discretionary spending. Expansive fiscal policy served to raise deficits in most countries, some of which faced further costs from stabilizing financial institutions, pushing deficits even higher. Sharp increases in deficits led in turn to escalating levels of government debt. Policy during the Recovery With fiscal drag weighing on growth and with private-sector deleveraging also holding back consumption and investment, monetary policy bore the brunt of supporting the economy. With policy rates at or approaching zero, central banks of necessity turned to unconventional policy tools such as large-scale asset purchases and enhanced forward guidance about the future path of policy rates. These unconventional tools have, in my view, served to support a recovery in domestic demand and, as a consequence, global economic growth. Even so, the recovery in most advanced nations has proceeded more slowly than policymakers would have hoped. This sluggishness has been due in part to the severity of the financial shock associated with the crisis and the persistent headwinds to recovery in its aftermath. But the lack of fiscal support for demand in recent years also helps account for the weakness of this recovery compared with past recoveries.1 In the United States, fiscal policy has been much less supportive relative to previous recoveries. For instance, at a comparable point in the recovery from the 2001 recession, employment at all levels of government had increased by about 800,000 workers; in contrast, in the current recovery, government employment has declined by about 650,000 jobs. Lessons A second lesson is that, while even if it is appropriate for fiscal policy to play a larger role when policy rates are near zero, policymakers nevertheless may face constraints in implementing fiscal stimulus. This means that central banks need to be prepared to employ all available tools, including unconventional policies, to support economic growth and to reach their inflation targets. A third critical lesson pertains to the importance of having a sound and resilient financial sector with strong capitalization and prudent risk management, supported by effective regulation and supervision. The recent crisis has appropriately increased the focus on financial stability at central banks around the world. At the European Central Bank (ECB), the recent comprehensive assessment is an important step toward building confidence in euro-area banks. I wish the ECB great success as it takes on its new responsibilities at the center of the single supervisory mechanism. At the Federal Reserve, we have devoted substantially increased resources to monitoring financial stability and have refocused our regulatory and supervisory efforts to limit the buildup of systemic risk. This macroprudential approach to promoting financial stability will be an important complement to our other tools for promoting a healthy economy. Looking Ahead Even so, I continue to anticipate that the headwinds associated with the financial crisis will wane. As employment, economic activity, and inflation rates return to normal, monetary policy will eventually need to normalize too, although the speed and timing of this normalization will likely differ across countries based on differences in the pace of recovery in domestic conditions. This normalization could lead to some heightened financial volatility. But as I have noted on other occasions, for our part, the Federal Reserve will strive to clearly and transparently communicate its monetary policy strategy in order to minimize the likelihood of surprises that could disrupt financial markets, both at home and around the world. More importantly, the normalization of monetary policy will be an important sign that economic conditions more generally are finally emerging from the shadow of the Great Recession. 1. See Greg Howard, Robert Martin, and Beth Anne Wilson (2011), “Are Recoveries from Banking and Financial Crises Really So Different?” International Finance Discussion Papers 1037 (Washington: Board of Governors of the Federal Reserve System, November). Return to text 2. See, for instance, Lawrence Christiano, Martin Eichenbaum, and Sergio Rebelo (2011), “When Is the Government Spending Multiplier Large?” Journal of Political Economy, vol. 119 (February), pp. 78-121; and J.Bradford Delong and Lawrence H. Summers (2012), “Fiscal Policy in a Depressed Economy,” Brookings Papers on Economic Activity, Spring, pp. 233-97. Return to text |

| Posted: 10 Nov 2014 02:30 PM PST My afternoon train reads:

What are you reading?

First-Time Home Buyers |

| Offshore Profits Avoid IRS Reach Posted: 10 Nov 2014 12:30 PM PST

|

| Posted: 10 Nov 2014 09:30 AM PST

|

| Apparently, You CAN Buy (Some) Happiness Posted: 10 Nov 2014 07:30 AM PST It looks as if you can buy happiness, after all. At least, in limited amounts, and up to a point. That seems to be the conclusion based on a recent survey by the Pew Research Center, part of the Pew Charitable Trust. Pew notes that Israel, the U.S., Germany and the U.K. have the happiest populations among advanced economies. This can be seen in the chart below:

It should come as no surprise that in the emerging-market countries, rising income tends to be associated with substantial increases in life satisfaction. Some of the biggest gains in self-perceived life satisfaction occurred in Indonesia, China, Pakistan, Malaysia and perhaps most surprisingly, Russia. Overall, the correlation between increasing income and happiness isn’t especially surprising to psychologists and economists who study the field. Continues here

|

| Posted: 10 Nov 2014 06:00 AM PST My morning train reads:

What are you reading?

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

0 comments:

Post a Comment