The Big Picture |

- Inflation Experience and Inflation Expectations: Dispersion and Disagreement Within Demographic Groups

- MiB Suggested Guests for 2015: A List

- 10 Monday PM Reads

- BBRG TV: Breaking Down 1.5 Billion Bonus Pool at Pimco

- Common Mythconceptions

- History of the Wealth Gap in Europe and America

- 10 Monday AM Reads

- Get It: Art of McCartney

- 2015 Is Shaping Up to Be a “Turkey” of a Year for the U.S. Economy and Stock Market

| Posted: 18 Nov 2014 02:00 AM PST

|

| MiB Suggested Guests for 2015: A List Posted: 17 Nov 2014 05:00 PM PST On Saturday, I asked for your suggestions for potential guests for Masters in Business here, and on Twitter as well. Here is what you suggested: Blog reader suggestions:

Twitter Suggestions:

|

| Posted: 17 Nov 2014 02:30 PM PST My afternoon train reads:

What are you reading?

Money Surges Into Shanghai Stocks on Stock Connect’s First Day

|

| BBRG TV: Breaking Down 1.5 Billion Bonus Pool at Pimco Posted: 17 Nov 2014 12:45 PM PST Pimco paid its former CEO Bill Gross a bonus of about $290 million in 2013, a year in which his Total Return Fund trailed a majority of peers, according to documents provided to Bloomberg View by someone with knowledge of Pimco's bonus policies. Bloomberg's Bloomberg View Columnist Barry Ritholtz speaks on "Bloomberg Surveillance." His opinions are his own. Source: Bloomberg, Nov. 14 2014 |

| Posted: 17 Nov 2014 11:00 AM PST

|

| History of the Wealth Gap in Europe and America Posted: 17 Nov 2014 07:30 AM PST Last week, we reported the ungodly sums of money the top executives at Pimco made. We also noted the obsession we have with tracking other people's wealth. Perhaps I painted with too broad a brush when I described this as an American pastime; to be more accurate, it is a hobby of the moneyed classes in general and on Wall Street in particular. My apologies to the rest of America, onto whom I unfairly projected this unseemly preoccupation. Still, endeavoring to understand how the current circumstances evolved is a worthwhile undertaking. Wealth, public policy and economic inequality developed along two very different paths in Europe and the U.S. That is where we begin our discussion this morning. I’m going to overly generalize and exaggerate a bit here to make a point about how society evolved in the U.S. and on the Continent. Modern Europe had a 1,000-year head start on America. By the time the first European explorers were taking tentative steps on the shores here, Europe had become a well-developed feudal society. If you want to consider extreme levels of income inequality, consider the distribution curve of property ownership in that system. Typically, the feudal lord or king owned, well, everything. Serfs were allowed to work the land, and most of the bounty went to the crown. They could hunt in the royal fields and forests, providing the appropriate tax was paid. The king provided some sort of justice as well as protection from marauding hordes. In exchange for these royal gifts, one only had to promise undying fealty, a willingness to be conscripted into the military for both needed defense and the occasional foreign involvement, or anything else at His Majesty's or His Lordship’s discretion. Let's not even discuss the right of primae noctis. |

| Posted: 17 Nov 2014 04:30 AM PST Once more into the breach, with the latest morning train reads:

|

| Posted: 17 Nov 2014 03:30 AM PST

After streaming this all for the past 4 days, I just ordered the new “Art of McCartney” 2 CD/1 DVD set from Amazon. The list of artists doing covers of Beatles/Wings/McCartney songs is fantastic:

I bet this will be a monster.

|

| 2015 Is Shaping Up to Be a “Turkey” of a Year for the U.S. Economy and Stock Market Posted: 17 Nov 2014 03:00 AM PST 2015 Is Shaping Up to Be a "Turkey" of a Year for the U.S. Economy and Stock Market

If relatively robust growth in thin-air credit was a major factor accounting for 2014's bountiful U.S. economic harvest, as I believe it was, then 2015's "harvest" is likely to be considerably less bountiful. Growth in thin-air credit has already begun to decelerate and is on course to further decelerate in 2015. As mentioned above, the Fed curtailed its purchases of securities more aggressively than I had reckoned a year ago and ended its purchase program in October 2014. Although bank credit has grown considerably faster than I had anticipated, it is not fast enough to compensate for the slowdown in the growth of Fed thin-air credit.

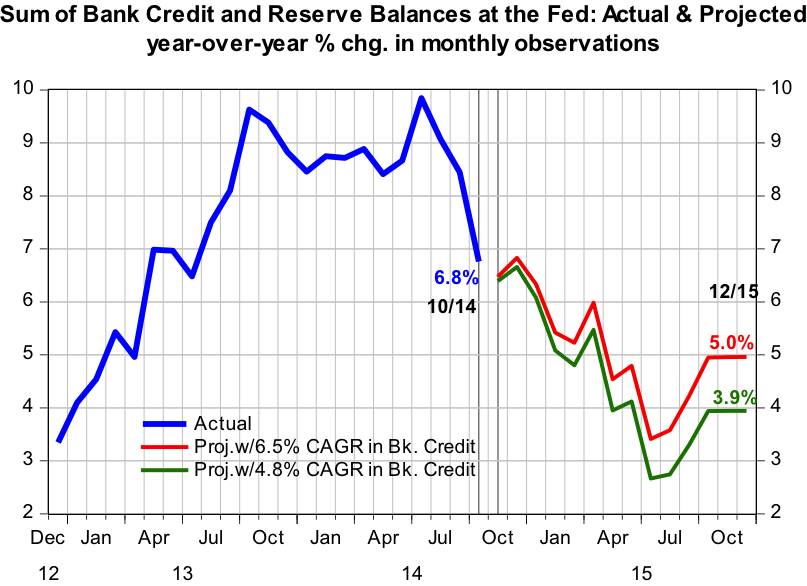

Plotted in the chart below are actual and projected monthly observations of year-over-year percent changes in the sum of commercial bank credit and reserves held by these banks and other depository institutions at the Federal Reserve. The actual data are through October 2014, with the projections running from November 2014 through December 2015. There are two separate projections, both of which assume that reserves held at the Fed (the Fed's contribution to thin-air credit) remain constant at the actual October level. When the Fed is not engaged in a quantitative easing (QE) policy, reserves of depository institutions held at the Fed typically grow less than 1% annually. In the 12 months ended October 2014, bank credit grew by 6.5%. So, in the first projection of thin-air credit growth, I assume that bank credit increases each month at a compound annual growth rate (CAGR) of 6.5% and reserves held at the Fed remain constant. In the 3 months ended October 2014, bank credit increased at a CAGR of 4.8%. So, in the second projection of thin-air credit growth, I assume that bank credit increases each month at a CAGR of 4.8% and, again, reserves held at the Fed remain constant.

After reaching a recent peak in growth of 9.8% in July 2014, year-over-year growth in thin-air credit decelerated to 6.8% in October 2014. A deceleration in growth of three percentage points in three months is severe in and of itself. But, wait. There is more, or less, as the case may be. With reserves at the Fed constant, if bank credit increases at a CAGR of 6.5% going forward, its October 2014 year-over-year increase, then the year-over-year growth in thin-air credit, i.e., the sum of bank credit and reserve balances at the Fed, will further decelerate to 5.0% by December 2015. With reserves at the Fed constant, if bank credit increases at a CAGR of 4.8%, its CAGR in the three months ended October 2014, then the year-over-year growth in thin-air credit will decelerate to 3.9% by December 2015. To put all of these growth rates into context, the median year-over-year change in monthly observations of the sum of bank credit and reserve balances at the Fed from December 1977 through December 2006 was 7.4%. As U.S. thin-air credit growth is on track to slow in 2015, thin-air credit growth in the eurozone and in Japan is likely to accelerate as the European Central Bank and the Bank of Japan step up their QE programs. These foreign QE programs could indirectly stimulate U.S. exports. But the dominant factor affecting the U.S. economy in 2015 will be below-normal growth in U.S. thin-air credit. So, as you gather your family around you on Thursday, November 27, to give thanks for our bountiful 2014 economic harvest, bear in mind that next year's harvest is likely to be a "turkey" in comparison.

Paul L. Kasriel |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

0 comments:

Post a Comment