The Big Picture |

- Gauging the Impact of the Small Business Lending Fund

- 10 Tuesday PM Reads

- Closer View of the Housing Boom

- Stop Making Intellectually Disingenuous Market Arguments

- 10 Tuesday AM Reads

- Falling apart: America’s neglected infrastructure (60 Minutes)

| Gauging the Impact of the Small Business Lending Fund Posted: 26 Nov 2014 02:00 AM PST Gauging the Impact of the Small Business Lending Fund

~~~~ The Small Business Lending Fund (SBLF) was created in 2010 to encourage small business lending by providing capital to qualified community banks. The Treasury provides banks with capital by purchasing Tier 1-qualifying preferred stock or the equivalent in each bank, with the intention that banks use this capital to make loans to small businesses. Community banks were targeted because they have traditionally supplied a significant share of the total amount of loans made to small businesses. For example, as of 2014:Q1, community banks held 45 percent of small business loans, according to the March FDIC Quarterly Banking Profile. We examine the first quarter of 2014 data to determine the extent to which banks that received funding have increased their small business lending. Institution-specific data on the change in small business lending to SBLF recipients is available on a quarterly basis from the US Treasury. To make it easy to compare before and after levels of lending, the Treasury calculated a baseline for comparison, which is defined as the average level of each bank's lending prior to receiving funds. A bank's baseline is the average of its qualified small business lending for each of the four quarters leading up to and ending on June 30, 2010. This applies for all banks that receive funding regardless of their entry date into the program. We compare banks' baseline lending to their lending in subsequent quarters up through 2014:Q1.

In the aggregate, small business lending has increased in every quarter since the banks received SBLF funds. As of 2014:Q1, mean lending was 142 percent higher than mean baseline lending for the whole sample. Banks pay for SBLF funds by means of the dividends they pay on the stock purchased by the Treasury. The dividend rate is reduced as their level of small business lending increases. The program incentivizes institutions to increase their lending immediately by creating a situation in which banks must use SBLF funds right away to ensure they are paying the lowest rate for them. Price Banks Pay (Dividend Rate) for SBLF Funds

Interesting trends are visible if we separate the banks by their initial baseline lending. Banks that were lending over $1 billion before the program did not experience increases until 6 quarters into the program, while banks with baseline lending less than $1 billion experience gains immediately. Bank size also determines differences in subsequent lending.

Banks with more than $20 million in baseline lending are comparable when looking at the change in their current lending over the starting baseline; banks below $20 million in baseline lending look rather different. This difference is due to many institutions receiving SBLF funds that were greater than their current levels of baseline lending. With the SBLF funds larger than their baseline, it was much easier to increase their lending over 100 percent or, in some cases, 400 percent. To observe small business lending growth for different regions of the United States, we focus on the first quarter of 2014 and break the data down by region. The Southwest experienced the largest increase over baseline lending—up 50 percent. The Midwest experienced the lowest increase in small business lending over mean baseline lending; yet its increase still reached 32 percent for the first quarter of 2014. All other regions experienced increases in lending as well.

The SBLF categorizes small business loans made in terms of the following types: commercial and industrial, owner occupied commercial real estate, loans to finance agricultural production, and loans secured by farmland. The majority of regional loans consist of commercial and industrial and owner occupied commercial real estate. Agricultural production and farmland loans are seen in the regional areas where we would expect farming to be a portion of small businesses.

While it is too early to evaluate the long-term effects of the SBLF program on small business lending, the data so far show that banks have used SBLF funds to increase their small business lending. Whether SBLF funding will play a long-term role in insuring small business lending continues to be available to qualified borrowers remains to be explored in further studies. ~~~ Kristle Romero Cortés |Research Economist  Kristle Cortés is a research economist in the Research Department of the Federal Reserve Bank of Cleveland. Her research interests include empirical corporate finance, entrepreneurial finance, and the structure, optimization, and regulatory practices of the financial services industry.

| ||||||||||||||||||||||

| Posted: 25 Nov 2014 01:30 PM PST My afternoon train reads:

What are you reading?

Rally in Treasuries Makes a Longstanding Bet Look Good

| ||||||||||||||||||||||

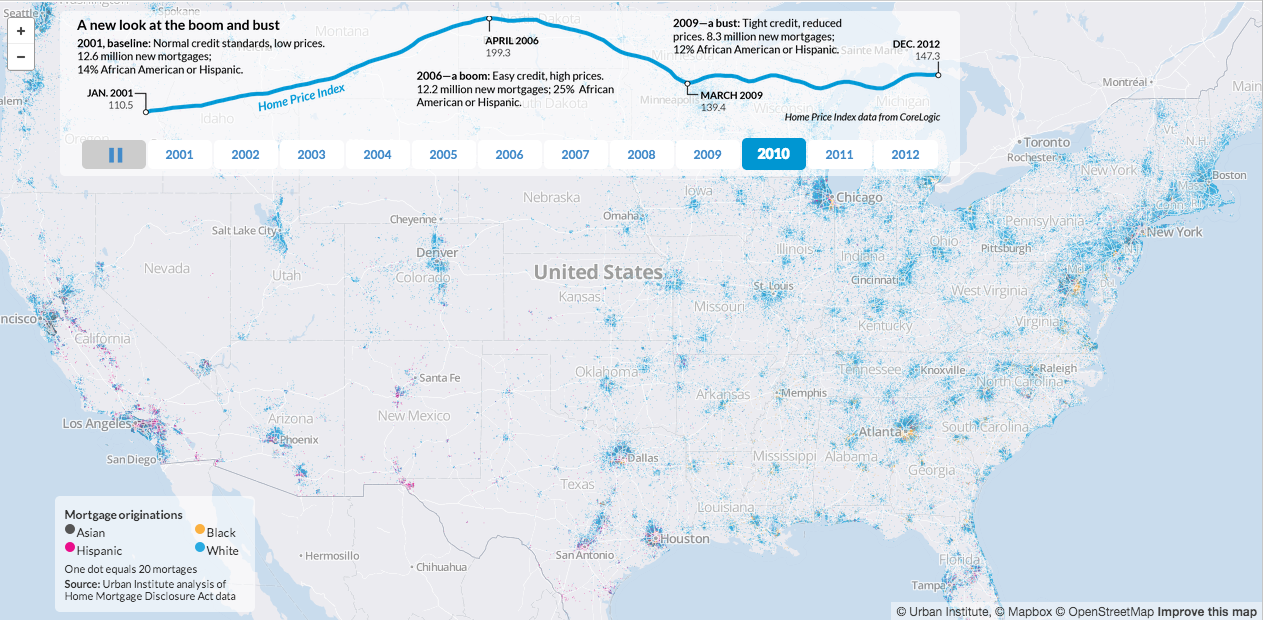

| Closer View of the Housing Boom Posted: 25 Nov 2014 09:00 AM PST Click to see the animated changes to the map. | ||||||||||||||||||||||

| Stop Making Intellectually Disingenuous Market Arguments Posted: 25 Nov 2014 05:30 AM PST The quality of our discourse is decaying. This was once a standard complaint about the tone and depth of our national political debate. Now it has spilled into the financial realm. Shall we blame Twitter, trolls or bloggers? I am unsure of the underlying reason. But as we have seen far too, financial discussions seem to entail people arguing at cross-purposes. Bull-bear debates devolve into winning the argument at any cost. Previously, we had a true competition of ideas in the marketplace. Now, we have discussions that range between disingenuous and useless. The hunt for the truth has been replaced by the search for bragging rights. Price discovery, like so many other things in our society, depends on a robust and open debate. The intellectual arguments can and do sway investors about their investment postures and positions. Efficient markets eventually find their way to proper pricing, but that "eventually" can take a long time. As John Maynard Keynes observed, "Markets can remain irrational longer than you can remain solvent." Perhaps a few examples might illustrate the point. In discussing the debate over gold, money manager Ben Carlson observes:

If you want to have an intellectually dishonest argument about gold, simply cherry pick the time line that supports your argument.

| ||||||||||||||||||||||

| Posted: 25 Nov 2014 05:00 AM PST My morning afternoon train reads:

| ||||||||||||||||||||||

| Falling apart: America’s neglected infrastructure (60 Minutes) Posted: 25 Nov 2014 03:00 AM PST Falling apart: America’s neglected infrastructure More videos after jump The politics of infrastructure ~~~ Cost of shutting down the Portal Bridge |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

0 comments:

Post a Comment