The Big Picture |

- Economists Discuss the Federal Reserve

- 10 Wednesday PM Reads

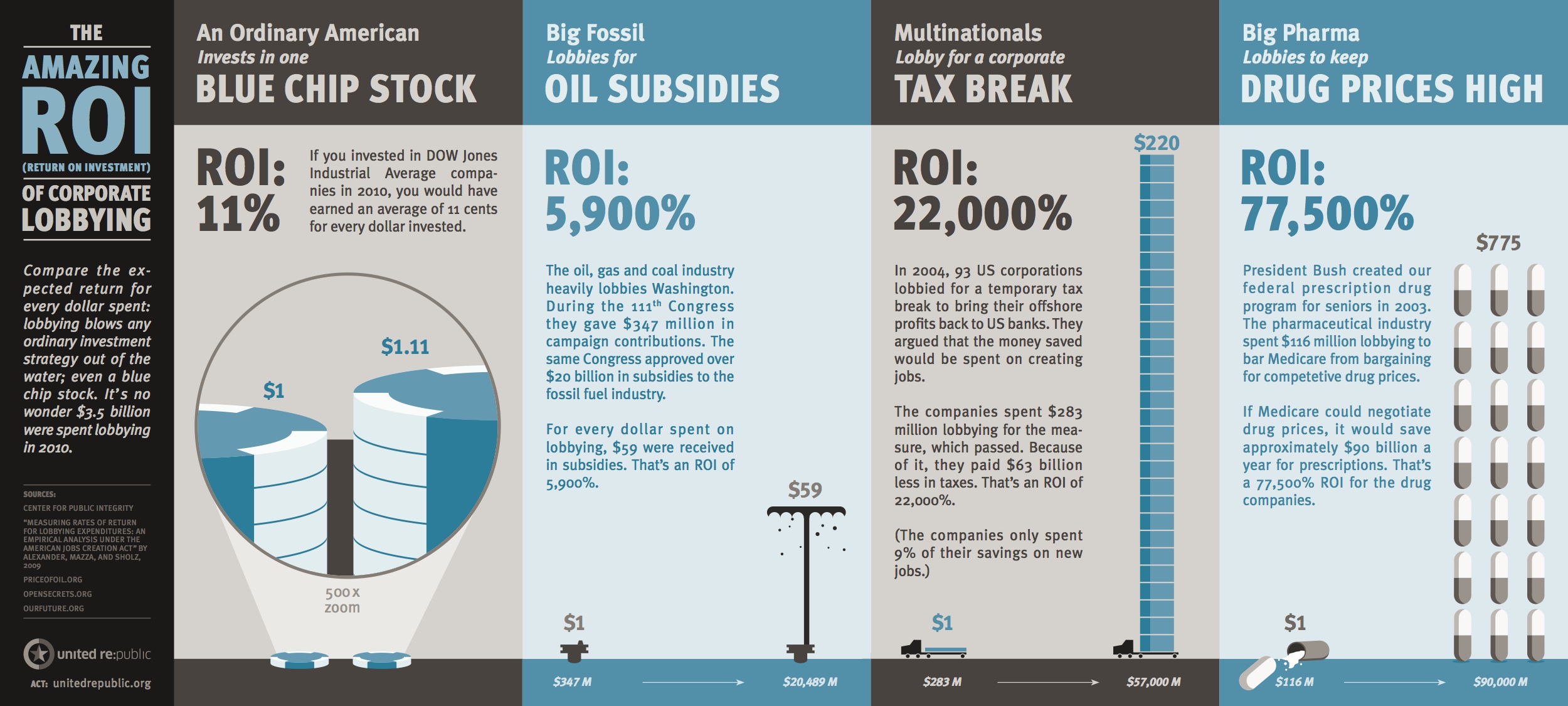

- ROI of Corporate Lobbying

- Merrill Lynch: Market Analysis Technical Handbook

- 10 Wednesday AM Reads

- Habits of the Bear, Bull Markets and Agency Issues

- China’s ‘ghost mall’

- Catching Falling Knives

- Birds and Dinosaurs

| Economists Discuss the Federal Reserve Posted: 16 May 2013 02:00 AM PDT Economists Michael Bordo, Marvin Goodfriend, Barry Eichengreen, and Allan Meltzer share their opinions on the Fed—past, present, and future. Watch Sandra Pianalto, Cleveland Fed president, comment on how the past informs present Fed policies: http://www.clevelandfed.org/annualreport Visit the Cleveland Fed’s channel for more videos: http://www.youtube.com/clevelandfed |

| Posted: 15 May 2013 01:30 PM PDT My afternoon train reads:

What are you reading?

Chart of the Day |

| Posted: 15 May 2013 11:30 AM PDT |

| Merrill Lynch: Market Analysis Technical Handbook Posted: 15 May 2013 09:00 AM PDT

I wish I could find a public link for this: Merrill Lynch just put out a very cool 60 page “primer” on Technical Analysis. It covers the core concepts behind technicals, including Trends, Relative Price Analysis, Price Momentum Indicators, Reversals, The importance of volume, Support and Resistance, Market Breadth Of course, you could always go out and buy Edwards & Magee’s Technical Analysis of Stock Trends, but you get a very different read from practitioners working at a major wire house. I have my own PDF (which I cannot post to Scribd for work product/copyright reasons), but if anyone knows of a public link, please share!

|

| Posted: 15 May 2013 07:00 AM PDT My morning reads:

What are you reading?

Currencies react to Bank of Japan's recent monetary moves |

| Habits of the Bear, Bull Markets and Agency Issues Posted: 15 May 2013 04:30 AM PDT

The above quote from Barron’s has been on my mind for a while. I thought of it again as the markets have made a series of new highs, and the bear community has been split. Some have been “forced in,” while others have doubled down. The context of the above was a letter to Barron’s in response to a December 1st 2012 Abelson commentary that stated “why money manager John Hussman is very bearish on stocks” (“A Real Cliff Hanger,” Up & Down Wall Street, Dec. 3) There is an intricate set of issues here, but I want to focus on three aspects: 1) Psychology, 2) Error admission & correction, and 3) why “Other People’s Money” (OPM) agency issue is not present or understood by the commentariat — those ministers without portfolio who are the background noise to the market. Since this rally began in March 2009, it has been disliked. I was a kid in 1973-74, so I have no firsthand recollection of how the crowd responded to the 76% bounce-back rally. 1933 was way before my time. Perhaps there was a touch of hyperbole when, back in 2009, I wrote this was the Most Hated Rally in Wall Street History®. I wasn’t present for these other similar crash bouncebacks, but I suspect the psychology was the same. Dispirited traders suffering from recency effects were overly impacted by memories of the crash. The rally left these frightened folks behind. That emotional cognitive bias has prevented many from recognizing the turn or even committing in a small way to having upside exposure. There area great many reasons why the rally should not continue, and why it will end badly. There certainly are plenty of things to be concerned about. However, what makes investing in markets so different from other forms of intellectual debate is that we regularly get a resolution to the different arguments. We may have different timelines, and the daily action is essentially noise, but we do get a resolution. Each month, each quarter, each year, we see which argument was more pragmatically correct in terms of the outcome of various risk assets. Their progress, or lack thereof, is the ultimate adjudicator. This is not to say that markets are never wrong — they often can be, and for extended periods of time. However, beyond the psychology we discussed above (and ad nauseum elsewhere), there comes a point were you must admit error, reverse your position, and move on. This is where the quote above comes in. If you are running OPM, you cannot miss a 145% move to the upside. The classic quote on this is “If you are bullish and wrong, your clients are angry at you. If you are bearish and wrong, they fire you.” Hence, our agency issue. This is what is meant by “Forced in” — managers running real assets cannot sit on the sidelines. Eventually, they either buy in or lose so much in AUM that they have effectively been fired. This is why having some form of self analysis to examine when you are wrong, to be able to determine why, and then reverse your position is so crucial to anyone who is an investor (professional or amateur). The exceptions are the Ministers without Portfolio. These are the talking heads, the pundits and strategists who can carve out an intellectual position that proves to be wildly wrong. And they can do so without penalty. Think about who is on TV and splling pixels on the OpEd pages. These People who have been wrong on everything from Equities to Bonds to the Dollar to Gold to Apple and back again. How is it this parade of wrong way Riegels manages to keep showing up and blathering about whatever? Is there no accountability? The answer is surprisingly simple: This is not a bug, its a feature. They are in the infotainment business, not the asset management business. Hence, being wrong, albeit entertainingly, is part of their jobs. I started as a trader, moved to research, eventually coming back around as a money manager. I can tell you first hand that being eventually right — Dow 6800, anyone? — only works if your are on the sidelines yelling at the players. Your obligations completely change once you step onto the field of battle. When you are responsible for people’s portfolios, your role must change. Note too, that this is not Chuck Prince’s dance when the music is playing. As CEO, his misaligned compensation encouraged him to dance right to the edge of the cliff. Some of us clearly put forward compelling analyses as to why that Housing/Derivatives/Subprime cycle was doomed. Which brings me back to the present market. What we are dealing with today is a case of first impression — massive credit crisis and collapse, followed by massive Fed intervention. We don’t know how this plays out, as we have never seen anything quite like this in history. Can the Fed simply wait it out, and let $4 trillion in bonds to mature without rolling over? I have no idea, but neither do the folks insisting it ends with us living in a post-apocalyptic Mad Max era. Just like every other cycle, one day, this bull market will end. I cannot tell you if its next Tuesday or sometime in 2019. The average (See first table below) is 3.8 years. We are now at 4.1 years. But the range is much broader, as both tables below makes clear. There are many silly reasons for being either all in — or all out — of the markets. The bottom line is that you should have a firm grasp on your own investment posture, risk tolerances and financial goals. You should understand how we got here and why. Make sure you have some form of your own coherent plan. But if you are waiting for someone else on TV to tell you what to do, whether its Jim Cramer or David Tepper or even lil’ ole Me, then you have yourself a big problem. There is asset management, and there is infotainment, and never the twain shall meet.

click for larger graphic

Previously: Four Stages of Secular Bear Markets (August 27th, 2009) The Most Hated Rally in Wall Street History (October 8th, 2009 Bull Market Durations (January 15th, 2013) Is the Secular Bear Market Coming to an End? (February 4th, 2013)

Table: Secular Bear Markets and Subsequent Rebound Rally: >

|

| Posted: 15 May 2013 04:00 AM PDT |

| Posted: 15 May 2013 03:00 AM PDT |

| Posted: 15 May 2013 02:00 AM PDT |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment