The Big Picture |

- Are the Wars in the Middle East and North Africa Really About Oil?

- 10 Monday PM Reads

- The Unemployment Surprise

- Mrs Merkel expected to receive a warm !!! welcome in Athens tomorrow

- Our Typical, Mediocre Post Credit Crisis Recovery…

- Another European coffee talk

- 10 Monday AM Reads

- Revisiting the Greenspan Legacy (circa 2008)

- A look inside the Space Shuttle Atlantis

- China Telecom Giant Huawei A Spy?

| Are the Wars in the Middle East and North Africa Really About Oil? Posted: 08 Oct 2012 10:30 PM PDT The Wars in the Middle East and North Africa Are NOT Just About Oil … They're Also About GASThe Iraq war was really about oil, according to Alan Greenspan, John McCain, George W. Bush, Sarah Palin, a high-level National Security Council officer and others. Dick Cheney made Iraqi's oil fields a national security priority before 9/11. The Sunday Herald reported:

The Afghanistan war was planned before 9/11 (see this and this). According to French intelligence officers, the U.S. wanted to run an oil pipeline through Afghanistan to transport Central Asian oil more easily and cheaply. And so the U.S. told the Taliban shortly before 9/11 that they would either get "a carpet of gold or a carpet of bombs", the former if they greenlighted the pipeline, the second if they didn't. See this, this and this. Congressman Ed Markey said:

Senator Graham agreed. And the U.S. and UK overthrew the democratically-elected leader of Iran because he announced that he would nationalize the oil industry in that country. It's a War for GASBut it's about gas as much as oil … As key war architect John Bolton said last year:

John C.K. Daly notes:

The Taliban visit to the U.S. has been confirmed by the mainstream media. Indeed, here is a picture of the Taliban delegation visiting Unocal's Houston headquarters in 2007:

U.S. companies such as Unocal (lead on the proposed pipeline) and Enron (and see this), with full U.S. government support, continued to woo the Taliban right up until 2001 in an attempt to sweet-talk them into green-lighting the pipeline. For example, two French authors with extensive experience in intelligence analysis (one of them a former French secret service agent) – claim:

Pepe Escobar notes:

Soon after the start of the Afghan war, Karzai became president (while Le Monde reported that Karzai was a Unocal consultant, it is possible that it was a mix-up with the Unocal consultant and neocon who got Karzai elected, Zalmay Khalilzad). In any event, a mere year later, a U.S.-friendly Afghani regime signed onto TAPI. India just formally signed on to Tapi. This ended the long-proposed competitor: an Iran-Pakistan-India (IPI) pipeline. Competing Pipe DreamsVirtually all of the current global geopolitical tension is based upon whose vision of the "New Silk Road" will control. But before we can understand the competing visions, we have to actually see the maps:

And here are the competing pipelines backed by the U.S. and by Iran, before India sided with the U.S.:

Iran and Pakistan are still discussing a pipeline without India, and Russia backs the proposal as well. Indeed, the "Great Game" being played right now by the world powers largely boils down to the United States and Russia fighting for control over Eurasian oil and gas resources:

The rising power China is also getting into this Great Game:

China is also pushing for an alternative to TAPI: an Turkmenistan-Afghan-China pipeline. Iran is also a player in its own right:

China's support for Iran is largely explained by oil and gas:

Why Syria?You might ask why there is so much focus on Syria right now. Well, Syria is an integral part of the proposed 1,200km Arab Gas Pipeline: Here are some additional graphics courtesy of Adam Curry:

So yes, regime change was planned against Syria (as well as Iraq, Libya, Lebanon, Somalia, Sudan and Iran) 20 years ago. And yes, attacking Syria weakens its close allies Iran and Russia … and indirectly China. But Syria's central role in the Arab gas pipeline is also a key to why it is now being targeted. Just as the Taliban was scheduled for removal after they demanded too much in return for the Unocal pipeline, Syria's Assad is being targeted because he is not a reliable "player". Specifically, Turkey, Israel and their ally the U.S. want an assured flow of gas through Syria, and don't want a Syrian regime which is not unquestionably loyal to those 3 countries to stand in the way of the pipeline … or which demands too big a cut of the profits. Pepe Escobar sums up what is driving current global geopolitics and war:

Postscript: It's not just the Neocons who have planned this strategy. Jimmy Carter's National Security Adviser helped to map out the battle plan for Eurasian petroleum resources over a decade ago, and Obama is clearly continuing the same agenda. Some would say that the wars are also be about forcing the world into dollars and private central banking, but that's a separate story.

|

| Posted: 08 Oct 2012 01:30 PM PDT My afternoon train reading:

What are you reading?

Bullish Sign for Stocks? Leverage Is Up |

| Posted: 08 Oct 2012 12:55 PM PDT The Unemployment Surprise

You Know You Were Surprised |

| Mrs Merkel expected to receive a warm !!! welcome in Athens tomorrow Posted: 08 Oct 2012 09:53 AM PDT Chinese services PMI rose to 54.3 in September, from 52 in August, according to HSBC/Markit. The official services PMI data came in at 53.7, lower than August’s 56.3. The HSBC data suggested that new orders rose at the fastest pace in 4 months, with employment rising. However, input price inflation also increased. Bloomberg reports that the services sector accounts for 43% of the Chinese economy, as opposed to 90% in the US, which the Chinese authorities want to raise to 47% by 2015, according to the Xinhua news agency; The World Bank has reduced E Asian growth to +7.2% this year ( down from +7.6% in May), from +8.3% in 2011 – still too optimistic. The IMF is likely to reduce its growth forecast at its annual meeting in Tokyo tomorrow. Reports of industrial strife at Foxconn’s plants in China. A number of businesses are thinking of relocating their operations out of China – the country is no longer the lowest cost producer. Chinese home prices are rising, albeit marginally, though for 3/4 months. However, inventory in the Tier 1 cities seem to be reducing and local governments are benefiting from increasing sales of land; Japanese auto sales in China are collapsing, following the dispute over certain islands in the South China seas. Korean manufacturers have gained materially – Hyundai’s sales rose by +9.5% Y/Y. Nissan’s sales, on the other hand, collapsed by 35% in September, as did Mazda’s; It looks as if Iran’s currency, the Rial is collapsing, with inflation soaring in the country. The sanctions are really having an impact. Cant see the Iranian economy improving, though Iran has significant forex and Gold reserves (US$70bn usable and 900 tons of gold), which will forestall an imminent collapse. The urban population, where most of the opponents to the current regime are based, are suffering, though the rural populations (supporters of the current regime) receive subsidies and are unaffected, at least for now. However, the effect of the sanctions may well stay possible military action by Israel, at least for a while; The Bundesbank has taken a swipe at the IMF, stating that the fund should not overstep its responsibility by suggesting proposals to deal with the economic challenges. I don’t think Mrs Lagarde will pay any attention;

The Euro Group finance ministers meet today. Still no solution on Greece, though Mrs Merkel is flying to Athens. Its clear that Mrs Merkel wants to help out Greece (certainly ahead of general elections in Germany in autumn next year), whilst her Finance Minister remains sceptical. I suppose Mrs Merkel does not want to explain to the Bundestag/a number within her own coalition, as to why funds provided by EZ countries needs to be restructured ie are unrecoverable. Having said that the risks continue to rise. Will Greece agree and then stick to its commitments – if you believe that, well……The opposition party (Syriza) is proposing that Greece default etc and is waiting in the wings. This situation will not hold, as the EU/Germany believe. Mrs Merkel will find it difficult, if not impossible, to provide further assistance for Greece, which they will need. Indeed, Mr Kauder, head of Mrs Merkel’s CDU has stated that there will be no Parliamentary majority for further aid to Greece. Finland and Holland will not play ball either. Going to be interesting. Still no deal on Spain either. PM Rajoy wants to wait for the impending regional elections at least and Germany wants all countries who need a bail out to be dealt at the same time, to avoid further problems with her Parliament. Mr Schaeuble stated that Spain does not need a bail out programme – really !!!!!!; Credit Suisse reports that there has been a sharp fall in Spanish Target 2 libailities in September. The ECB’s OMT seems to be having a positive impact, with material capital inflows into Spain last month – the 1st time that’s happened for a very long while. In addition, a number of funds are believed to have been buying Spanish, Italian and Portuguese debt, in particular. This is, indeed, good news if it continues; EZ sentix investor confidence index came in at -22.2 in October, better than -23.2 in September, though weaker than the -20.8, forecast by Reuters; The head of the ESM Mr Regling reports that the fund is up and running with a capacity of E200bn at present – the eventual size is expected to increase to E500bn, though likely more as the ESM leverages itself. He also talked about first loss guarantees – seems that they are looking at “guaranteeing” the return of principal of applicable EZ peripheral debt; German August industry output declined by -0.5% in August M/M (+1.2% in July), though better than the forecast of -0.6%. Y/Y, production declined by -1.2%. The current forecasts for Germany remains somewhat optimistic and further downgrades are likely. The German economy minister reported that factory orders declined by -1.3%, though exports rose by +2.4% in August, the 2nd consecutive monthly rise, well above the -0.6% decline expected. The German economy is likely to stagnate, at best, for the 2nd half of the year; A crisis between the UK, in particular, and the rest of the EU looks as if it will escalate. The British PM has threatened to veto the proposed increases. The EU is looking to increase its budget – well the price of caviar and Champagne gas gone up after all !!!. The EU is isolated given the politics in the EU. A 2 tier system is likely, with those in the Euro contributing more, whilst those outside, such as the UK, less. Given domestic politics and increasing EU scepticism in the UK, Mr Cameron cannot agree to a higher budget; The UK’s Office for Budget responsibility (“OBR”) looks as if it will advise the UK government that it will need to plug quite a large gap in public finances – some Sterling 15bn. As a result, the current austerity measures will need to be in place till 2018. Whoops – not going to go down well. (Source FT); The initiative by the Chinese telecoms equipment manufacturer, Huawei, for US authorities to review their business looks as if its backfired. The US House Committee on Intelligence stated that risks associated with Huawei and a smaller company ZTE “could undermine core US national security interests”. A definite whoops; President Hugo Chavez won the Presidential election in Venezuela – no great surprise, but he remains President for 6 more years – oh dear. However, Mr Chavez is ill and had to undertake extensive surgery recently. His opponent took only 45% of the vote. Polls prior to the elections, suggested that his opponent, Mr Capriles was neck and neck with Chavez. Whatever, the Venezuelan economy is tanking and change will happen, sooner rather than later; Outlook Gloomy day today as Asian markets turned lower on a weaker economic outlook and European markets sold off on recurring concerns with the EZ peripheral debt crisis. US markets are weaker. The Euro is weaker at US$1.2984. Gold is trading at US$1775, with oil at US$111.62, off as well, though still far too high. Negative news around. No real impetus to buy the markets. Complacency remains, with the VIX at 15.31, though nearly 100bps up from Fridays close. I just don’t believe that the current calm in the EZ will hold – yes winter is coming which suggests fewer demonstrations, but by next spring…..There are some positive aspects in the EZ it must be said – the current a/c’s of countries such as Greece and Spain are improving dramatically, though mainly due to lower demand. However, their debt positions remain unsustainable. Playing for time is the name of the game, though without some growth, this policy looks as if it is past its sell by date. However, with the major Central banks pumping liquidity into the system and ready to act further if necessary, its difficult to short. Much better to play the currencies – still don’t like the A$, Rand and Euro. Continue to watch (even more closely) the Yen. A very good friend of mine, Vicky Pryce, who was one of the chief economists for the UK government, amongst numerous other achievements, has written a book on the Greek crisis. The title is “Greekonomics The Euro crisis and why politicians don’t get it”. Vicky and I, it must be said, do not necessarily agree on Greece (we normally agree on most issues), but she makes compelling arguments to support her case. In addition, I nearly always read the views of people who differ from mine – far better in my view. Its a great read and I certainly would recommend it highly. Still in New York – will be her for another week at least. The US remains the best dirty shirt around, as Mr Gross of PIMCO puts it. Personally, I believe that the US, assuming the fiscal cliff issues are dealt with, is doing (much?) better than people think. The residential housing market remains the key. Kiron Sarkar 8th October 2012 |

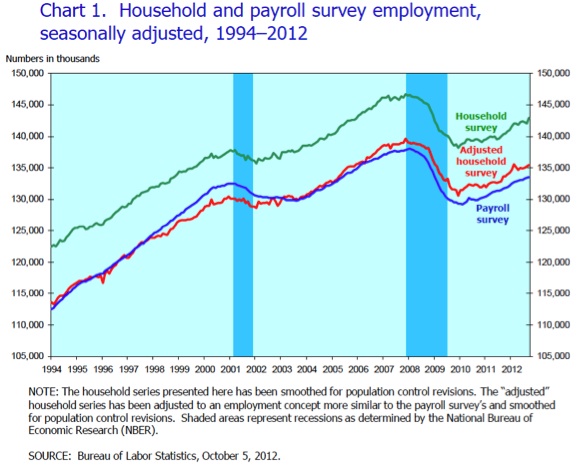

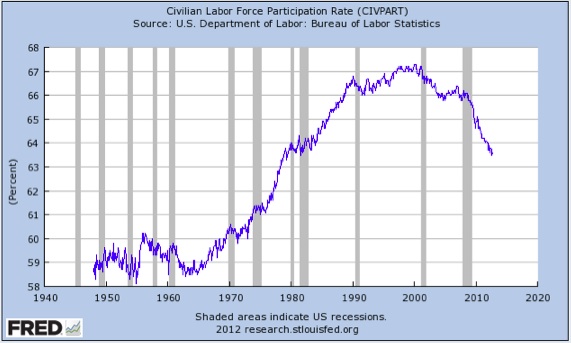

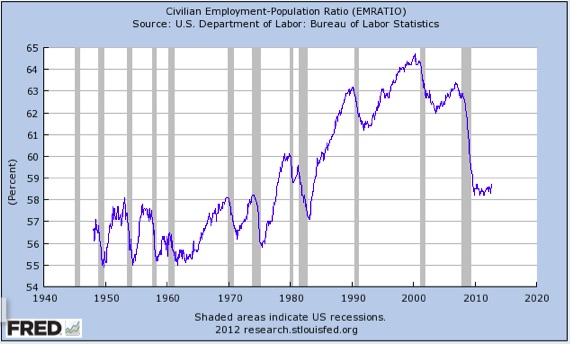

| Our Typical, Mediocre Post Credit Crisis Recovery… Posted: 08 Oct 2012 08:30 AM PDT

It is the silly political season, and while each side levels accusations at each other, neither wants to admit the simple truth: Both political parties helped to create the credit crisis (In Bailout Nation, I put it about 55/45). The Obama administration underestimated the depth of the recession, and failed to respond appropriately. Instead, he put two wholly unqualified people into senior positions: Tim Geithner, who failed upwards from the President of the NY Fed to become Treasury Secretary; And Lawrence Summers, who failed upwards, well, for most of his career. When he was Treasury Secretary, he helped pass the ruinous Commodity Futures Modernization Act of 2000, and helped to repeal Glass Steagall. Both were proteges of Robert Rubin. On the other side, of the political aisle, the Romney camp wants to blow up every negative data point into the world’s worst recovery. (Its not a typical recovery, and even by that standard its not the worst ever). What we have is a typical post-credit crisis recovery. Sub-par GDP, mediocre jobs recovery. As the monthly payroll chart at top shows, things have gotten better — just at a pace that is far less rapid than we prefer. Unless we are willing to pull out all of the stops — huge overseas tax free repatriation plus a massive Keynesian spending surge, we should expect more of the same. |

| Posted: 08 Oct 2012 07:56 AM PDT Ahead of another European Finance Minister coffee talk today, eyes are on the pressure the Spanish government will likely get to stop playing games on the day the Europeans are supposed to roll out their new bailout toy, the ESM. It supposedly has amazing powers of suspending reality for periods of time. Greece will be the other story as it seems they will get further leeway from their sugar daddies who will never get paid back all of what’s owed to them but for now will pretend to. German IP in Aug fell .5%, a touch better than estimates of a decline of .6%. Exports in Aug were unexpectedly higher by 2.4% m/o/m vs the estimated drop of .6%. After a vacation last week, the Shanghai index traded lower by .5% notwithstanding a rise in the HSBC private company weighted PMI services index to 54.3 from 52, a 4 month high. While the state company PMI last week fell sharply, at 53.7 is now more in line with HSBC. |

| Posted: 08 Oct 2012 07:00 AM PDT My reads to start off the week:

What are you reading? > Silicon Valley’s Stock Funk |

| Revisiting the Greenspan Legacy (circa 2008) Posted: 08 Oct 2012 05:30 AM PDT One-Two Punch: Who Did More Damage to the US Economy, Greenspan or Rubin?

Four years ago today, Peter Goodman of the NYT published this article about former Fed Chair Alan Greenspan, titled Taking Hard New Look at a Greenspan Legacy. After listing folks like Warren Buffett and George Soros and Felix Rohatyn who thought derivatives were far too dangerous to allow unfettered trading, one man took the other side of the deregulatory argument — Alan Greenspan:

The whole article is worth reading. It reflects the early days of the unraveling of the Maestro’s reputation, whose fall from grace accelerated as the crisis wound on. Today, it lay in ruins, where it deserves to be. Few men have wrought more economic damage in the misguided pursuit of a bad economic idea then former Fed Chief Alan Greenspan. No, as it turns out, neither Banks nor Markets can regulate themselves . . .

Source: |

| A look inside the Space Shuttle Atlantis Posted: 08 Oct 2012 05:00 AM PDT |

| China Telecom Giant Huawei A Spy? Posted: 08 Oct 2012 04:00 AM PDT Chinese telecom giant’s pursuit of building the next generation of digital networks in the U.S. prompts outcry in Washington. Steve Kroft reports. Huawei probed for security, espionage risk Huawei probed for security, espionage risk |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment