The Big Picture |

- By the numbers: The Demise of PCs

- How to Win at Forecasting

- Science Of Persuasion

- How important is the fiscal cliff for investors? Hint: Not very

- Student and auto loans still driving consumer credit gains

- Weekly Eurozone Watch (12/7/12)

- First Look: BMW 4 Series Coupe Concept

- US in Recession Since July?

- 10 Weekend Reads

- California Youth Crime Plunges to All-Time Low

| By the numbers: The Demise of PCs Posted: 08 Dec 2012 01:00 PM PST |

| Posted: 08 Dec 2012 11:30 AM PST Fascinating discussion over at Edge about the nature of expert judgment and what it means. (It careens into a little HedgeHog and Fox arguments). This has an enormous relevancy for investors. Here’s the intro, plus a link to the video. How to Win at Forecasting

Source: Edge

~~~ Philip E. Tetlock is Annenberg University Professor at the University of Pennsylvania (School of Arts and Sciences and Wharton School). He is author of Expert Political Judgment: How Good Is It? How Can We Know? Which describes a twenty-year study in which 284 experts in many fields, including government officials, professors, and journalists and ranging from Marxists to free-marketeers, were asked to make 28,000 predictions about the future. He found they were only slightly more accurate than chance, and worse than simple extrapolation algorithms. The book has received many awards, including the 2006 Woodrow Wilson Award from the American Political Science Association and the 2008 Grawemeyer Award for Ideas Improving World Order. |

| Posted: 08 Dec 2012 08:08 AM PST Animation describing the Universal Principles of Persuasion based on the research of Dr. Robert Cialdini, Professor Emeritus of Psychology and Marketing, Arizona State University. Dr. Robert Cialdini & Steve Martin are co-authors (together with Dr. Noah Goldstein) of the New York Times, Wall Street Journal and Business Week International Bestseller Yes! 50 Scientifically Proven Ways to be Persuasive.

|

| How important is the fiscal cliff for investors? Hint: Not very Posted: 08 Dec 2012 07:30 AM PST How important is the fiscal cliff for investors? Hint: Not very

The "fiscal cliff" paranoia continues unabated. Apparently, it is the only thing that matters to the markets. Every twist and turn in the negotiations is crucial to the future of the republic! Whenever the media obsess over a potential crisis, history teaches us that it is most likely to be overwrought hype. Recall the Y2k frenzy as Exhibit 1 in The People v. Really Bad Media prosecution. Want to learn just how absurdly obsessive the media have become over this? Just type "fiscal cliff" into Google Trends and you will see how, post-election, the term's appearance in the media simply went ballistic. Where did this sudden spike in mentions begin? The Columbia Journalism Review points to coverage such as that of the financial network CNBC. Ryan Chittum, who reports on the business media for CJR, notes that CNBC began a campaign called Rise Above that blanketed its airwaves since the day after the election with pleas for a solution to the fiscal cliff. As Google's trend chart shows, it was part of a media dogpile — at least until the David Petraeus affair sent the drones scurrying after a more salacious story. What does the fiscal cliff mean to investors? Let's start with a definition: The term refers to the deal that Congress made in late 2011 to temporarily resolve the debt ceiling debate. The "sequestration," as it is known, calls for three elements: tax increases, spending cuts and an increase to the payroll tax (FICA). The Washington Post's Wonkblog has run the numbers and finds "$180 billion from income tax hikes, $120 billion in revenue from the payroll tax, $110 billion from the sequester's automatic spending cuts and $160 billion from expiring tax breaks and other programs." That is a not-insignificant amount of money, but it is hardly the end of the world. To put this into context, it is a little less than the TARP bailout for Wall Street in 2009 and somewhat less than the American Recovery and Reinvestment Act, President Obama's stimulus package. An educated guess puts this at about $600 billion to $700 billion out of a $15 trillion U.S. economy. I'd ballpark that at about 4 percent of the GDP, or 0.50 percent of the forecasted GDP growth of 2 percent for calendar year 2013. The term "fiscal cliff," popularized by Fed Chairman Ben Bernanke, is really a misnomer. As several analysts have correctly observed, the effects of sequestration are not a Jan. 1, 2013, event. The impact of the spending cuts and tax hikes would be phased in over time. A fiscal slope is more accurate. Additionally, as students of history have learned, single-variable analysis for complex financial issues is invariably wrong. Because of the inherent complexity of economies and markets, we cannot adequately explain or predict their behavior by merely looking at just one variable. Given all this, what else might be driving equity markets? Consider the following factors as the causes of recent volatility: Weak corporate profits: If you want to understand market jitters, look no further than falling earnings growth. Profits and revenue have disappointed in the third quarter, coming in below estimates. As the Wall Street Journal noted, this has been the "worst quarter for corporate profits in three years." Even worse, future estimates for earnings growth keep sliding. In July, estimates for fourth-quarter profit were annualized gains of 14 percent. By October, that fell to 9.6 percent. It has now slipped to 5.5 percent, according to S&P Capital IQ. Markets got ahead of themselves: For the first three quarters of the year, the markets put up impressive numbers, with the S&P 500-stock index gaining 17 percent, and the tech-heavy Nasdaq running up over 23 percent. Those are great numbers versus historic average gains of 10 to 11 percent. Given the mediocre post-credit crisis recovery and the softening earnings growth, perhaps markets simply got too far ahead of themselves. Wall Street bet wrong on the elections: Lots of people seem to be saying that recent market turmoil is based on the financial community's evaluation of a possible deal between the White House and Congress. Do not pay much attention to Wall Street's assessment of politics. Let me remind you that the Street made very heavy bets on Mitt Romney winning the election. This was both in the campaign donations made by Wall Street firms as well as how fund managers and traders positioned their portfolios. They all misread what turned out to be an Obama electoral college blowout of 332 to 206. The sell-off since the election is as much about how a mispositioned Street was reversing itself as anything else. Those are probably the three largest factors. Of course, the euro-zone sovereign debt crisis is unresolved, and most of Europe is in a recession. In Asia, growth has been slowing, especially in China and India. And then there is the decreasing impact of Federal Reserve interventions in the markets. We seem to be getting less bang for the buck with each subsequent QE. I submit that all of these other factors are weighing much more on equity markets than the fiscal cliff. I am much more concerned about declining earnings and what they mean for the possibility of a recession in 2014. You should be, too. ~~~ Ritholtz is chief executive of FusionIQ, a quantitative research firm. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. On Twitter: @Ritholtz. |

| Student and auto loans still driving consumer credit gains Posted: 08 Dec 2012 06:30 AM PST In the just reported consumer credit data released by the Fed, revolving credit outstanding on a seasonally adjusted basis rose $3.4b m/o/m to $857.6b. That is the highest since May but looking at a longer term chart reflects more bouncing along the bottom. While nominal GDP growth is at new highs, revolving credit outstanding remains 16.5% below the ’08 record highs. AMEX CEO said it best this week at a conference that the US consumer is “generally reluctant to borrow” and “not demonstrating a desire or willingness to increase that debt burden.” On the nonrevolving side of credit outstanding, debt is at an all time high and that’s been mostly driven of late by student loans outstanding. Student loans held at the Fed’l Govt have increased from $104b in 2008 to $516b in Oct ’12. Also boosting the nonrevolving credit side of late has been the increase in auto loans which cheap credit from the Fed has helped to engineer at the same time the ABS market has come back to life in the search for yield. |

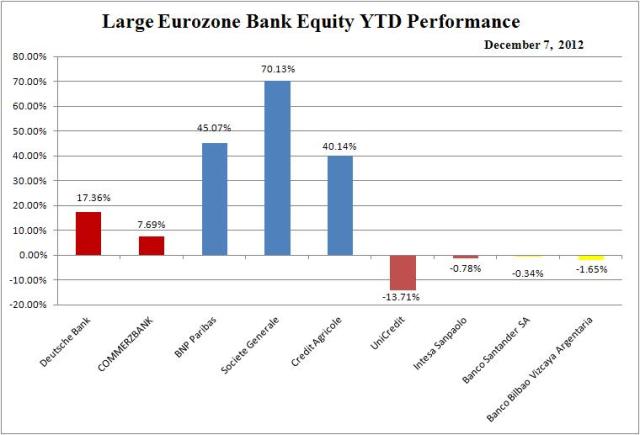

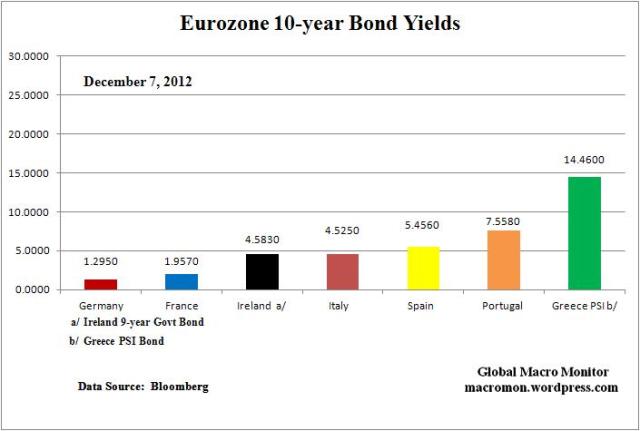

| Weekly Eurozone Watch (12/7/12) Posted: 08 Dec 2012 05:30 AM PST Key Data Points Comments Source: Guardian and Telegraph

(click here if charts are not observable)

|

| First Look: BMW 4 Series Coupe Concept Posted: 08 Dec 2012 05:00 AM PST A little bigger than the 3 series, with some more attitude and ridiculous 20″ wheels that will never make it to the final version:

Lots of photos to follow . . .

Source: Automobile Magazine |

| Posted: 08 Dec 2012 04:00 AM PST Lakshman Achuthan, Economic Cycle Research Institute, says the U.S. has been in a recession since July

|

| Posted: 08 Dec 2012 04:00 AM PST My longer form readings for your weekend enjoyment — this may be my favorite list in a long time:

What are you reading?

Apple’s Power Within

|

| California Youth Crime Plunges to All-Time Low Posted: 08 Dec 2012 03:00 AM PST |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment