The Big Picture |

- Clustered Housing Cycles

- Physics Envy and Economic Theory

- 10 Midweek PM Reads

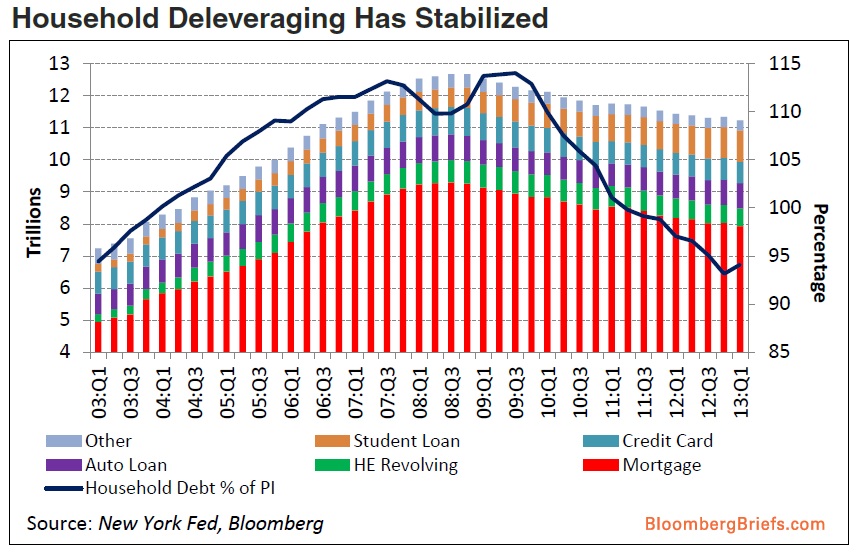

- Following the Fed Out of Bonds?

- 50 Year Chart: Stocks, Bonds & Gold

- 10 Mid-Weeks AM Reads

- Helicopter Ben Miscommunicates

- If Jupiter Were As Close as The Moon

| Posted: 27 Jun 2013 02:00 AM PDT |

| Physics Envy and Economic Theory Posted: 26 Jun 2013 04:30 PM PDT Economists were seduced by physics because it made their claims seem more scientific. Their belief was in the concept of equilibrium, in which it would be impossible to profit from trading around a circle of goods or a circle of currencies without actually producing anything. Of course, that is possible, and that did happen, and that’s because you’re never really at equilibrium.

Transcript after the jump

So I got pulled into economics in 2007 because of the 2008 economic crisis. Mike Brown who had been the first CFO of Microsoft, Chief Financial Officer of Microsoft and treasurer of Microsoft, he came to Toronto in 2007 and took my wife and I out to dinner and said he was trying to put together a research group to work on economics and he would like me to be involved. And I said, “I don’t know anything about economics.” And he said, “That’s okay because nobody does and the whole system is about to collapse.” He said, “The balance sheets of all the big investment banks — it’s like they have cancer. They’re full of holes.” And I remember being very struck by this because this was before anybody was talking about this. And so I started to meet with a group of people that he was pulling together to understand what was gonna happen and to understand if there was any way to save the situation. It was a very ambitious thing and, of course, we failed. But along the way I was motivated as a kind of public service to get interested in economics. And what I found . . . economics, in a way, is very easy for a physicist to understand because it’s very mathematical. And the mathematical models that they use are very clean. They’re based on assumptions and hypotheses, and you can study them. And as I studied it I began to understand, some for myself and more from just reading around because the faults with the standard economic models, with the standard models of finance, are well known. They have been in the literature for decades and decades. So let me give some examples. The standard model of economics is called the neoclassical model and it assumes that markets or systems where trading happens between consumers and firms and there’s certain simple models of how that goes on. And the ideas that these come to equilibrium. Equilibrium not in the physical sense but in special economic sense in which you reach a point at which the prices are fixed such that market forces fix the prices such that you maximize the happiness of the consumers and maximize the profits of the firms. And in so called equilibrium nobody can become happier or more profitable without somebody else becoming less happy or less profitable. And the ideology behind this — not behind the mathematics because mathematics doesn’t have an ideology — but behind the arguments that were made and still are made from this model is that markets don’t need regulation because they have these natural equilibria where everybody benefits to the maximum possible. And if you’re in equilibrium you can’t do better. Now there’s a fault with this and it’s an obvious fault and it’s been known since the 1970s from some theorems proved by some economists including some of the founders of this field of mathematical economics, which is that there’s not one equilibrium, there are many equilibria. In fact, there’s a vast number of equilibria. And so which equilibria, even assuming that this is a decent model of the economy which is not clear, but even assuming it’s a good model, which equilibria you’re in depends on the past history, it depends on regulation, it depends on politics, it depends on taste, it depends on changing taste, changing preferences. And so history matters and what’s called path dependence matters. This takes us outside the neoclassical model of economics but it doesn’t take us outside of economics because some wiser economist, for example, Brian Arthur had for years been developing models and theories of path dependent economy where the history does matter. People from the area of complex systems like Stu Kauffman, Prubac in developing models of markets where the history matters, where there’s not a single equilibrium, where there are many equilibria. And where change is paramount. Another symptom of this is the idea that arbitrage isn’t, I mean, in these neoclassical models when you go to equilibrium, arbitrage is impossible. Arbitrage is making a profit from trading around a circle of goods or a circle of currencies without actually producing anything. And in equilibrium that’s supposed to be impossible but lots of firms and investment banks made fortunes off of currency trading, so why is that? It turns out because you’re never really at equilibrium… Remainder of transcript: http://bigthink.com/videos/how-bad-sc… |

| Posted: 26 Jun 2013 01:30 PM PDT My afternoon train reading:

What are you reading? |

| Following the Fed Out of Bonds? Posted: 26 Jun 2013 11:30 AM PDT Click to enlarge

Excellent explanatory chart from the FT.

Source: |

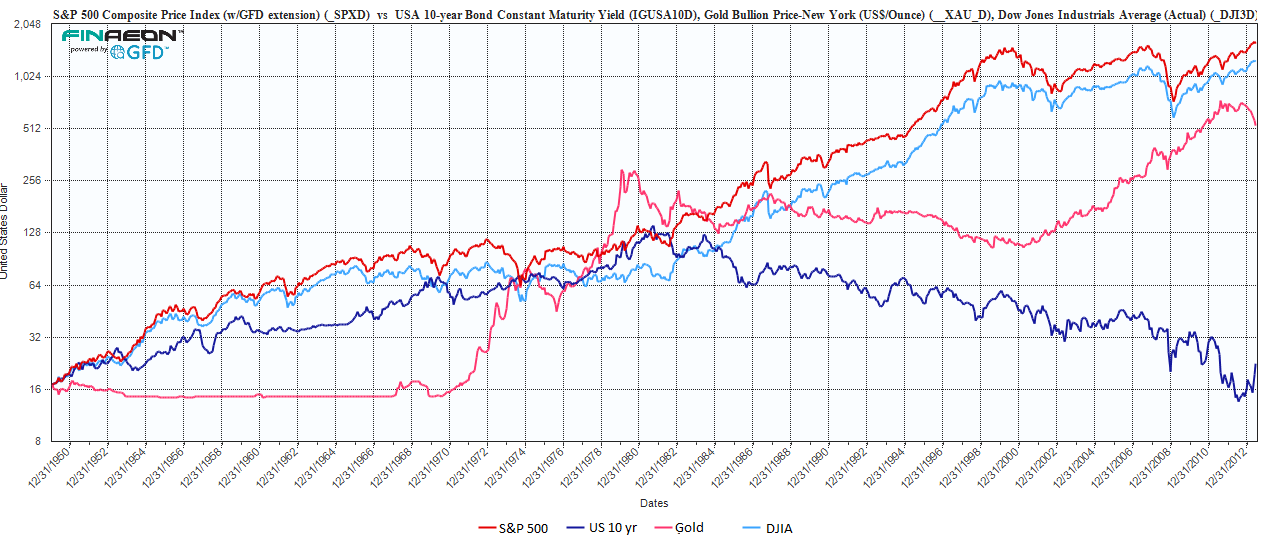

| 50 Year Chart: Stocks, Bonds & Gold Posted: 26 Jun 2013 08:30 AM PDT Click to enlarge

Yesterday, in response to our post on how wrong the public was back in this 2011 Gallup poll, the following suggestion was made:

The charts above date from 1950 to present. Its pretty clear that Gold moves in fits and starts; the Treasury market has had an enormous and unusual bull market, and stocks are volatile gainers over the long haul.

Source: |

| Posted: 26 Jun 2013 06:45 AM PDT My morning reads:

What are you reading?

Chart of the Day |

| Helicopter Ben Miscommunicates Posted: 26 Jun 2013 04:15 AM PDT The following commentary comes from my friend and colleague Stephan Weiss:

Last week at least started well as the upper echelon of fund managers heard from their "well-placed sources" that Helicopter Ben had miscommunicated the FOMC position when he spoke about tapering and would set the record straight at his press conference, imbuing them with the fortitude to get long in front of Wednesday afternoon. Well, they got half the story right as he did set the record straight. Taken alone, the FOMC minutes were positive for the market as nothing indicated that policy was going to change course. The indices acted accordingly, swaying between green and red. Then we found out that those sources were no more well-placed than a convertible parked beneath a tree with hanging bird feeders. First, the FOMC projections were released showing that the targeted 6.5% unemployment rate was now forecast to occur in 2014, not 2015, and that GDP growth was accelerating. Then, just prior to the reporter from TMZ asking Bernanke about his personal plans, his prepared remarks were released. Therein, Helicopter Ben dropped not more cash, but the bomb:

So here we are: the transparency thing as Bernanke explained the Fed's thought process. The FOMC will apparently begin to cut back this year and, depending upon the next jobs number, may do so before the third quarter ends. The point that we reach 6.5% has been moved up but that is no longer the trigger; now it is 7% accompanied by an upward bias in the economy and inflation at 2%. If only the Fed kept that information to themselves we could have read the minutes and gone on our merry way as the market stabilized and perhaps moved higher. Instead, traders relied traditionally unreliable FOMC forecasts – a flawed strategy in itself – and panicked. In the old days, pre-openness, the market took the real hit when the rate increase actually occurred and usually upon the move deep into neutral policy territory. That was decidedly less disruptive to the markets in terms of duration because by the time the liquidity geyser slowed to a drip, the economy was already on better footing, earnings growth was apparent and valuation could withstand less accommodative policy. But this is the worst of all worlds since we likely won't see much growth in earnings this quarter, Europe is still uncertain and China is on the verge of a credit crisis that will make 2008 look like boom times. Interbank lending rates in China have ballooned from just over 3% a month ago to over 11. Put in perspective, US rates are near zero. I can't imagine too many visitors to Jimmy Dean's factory leave the tour and buy a few links in the souvenir shop, anxious to cook them up when they get back to the trailers. Seems like traders feel the same way about the Fed post press conference, puking out their stocks and bonds, violating important levels of support. However, once the vision fades and their stomachs settle, a curing period that will likely take us through the next jobs number on July 5th (a light attendance day in the midst of a "4 day" weekend making for Über volatility), earnings and up to the next FOMC meeting, they will recognize a great buying opportunity– at least for stocks. Bonds, unfortunately, will stay in the grinder. For now, though, the carnage, bred through emotion, is likely done as atrophying now takes over. Within that time frame there will be peaks and valleys as volatility, courtesy of Fed transparency, becomes the norm. I'm up for nibbling for the intermediate and long term but the market hasn't corrected enough to find many real values. ~~~ Stephen L. Weiss has been on Wall Street for 25 years in senior positions at the industry's most prestigious asset management and investment banking firms. A former tax attorney, Weiss worked at Oppenheimer & Co. then Salomon Brothers during the time it was controlled by Warren Buffett, developing and communicating investment ideas to the industry's most respected investment funds including SAC Capital (Steve Cohen), Tiger Management (Julian Robertson), Soros Funds, Kingdon Capital and Omega Advisors (Lee Cooperman). Prior to joining Lehman Brothers to run equity sales he worked for Steve Cohen at SAC Capital. The managing partner at Short Hills Capital Partners, LLC., Steve has written three books and appears regularly on CNBC’s Fast Money Halftime Report. More information is available at www.shorthillscap.com.

|

| If Jupiter Were As Close as The Moon Posted: 26 Jun 2013 03:00 AM PDT Click to enlarge

See the full run of planets as if they were as close as the Moon at Daily Mail |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment