The Big Picture |

- Why Is the Job-Finding Rate Still Low?

- Why Trolls Start Flame Wars . . .

- 10 Tuesday PM Reads

- Income Distribution Like You Have Never Seen It

- Mobile Usage Trends, Illustrated

- 10 Tuesday AM Reads

- The Putin Put: Ukraine Dragging Down Your Portfolio?

- Nenner: Dow 5,000 in 2013

- Who’s Borrowing Now? Change in Debt by Credit Score and Age Group

| Why Is the Job-Finding Rate Still Low? Posted: 05 Mar 2014 02:00 AM PST Why Is the Job-Finding Rate Still Low?

Fluctuations in unemployment are mostly driven by fluctuations in the job-finding prospects of unemployed workers—except at the onset of recessions, according to various research papers (see, for example, Shimer [2005, 2012] and Elsby, Hobijn, and Sahin [2010]). With job losses back to their pre-recession levels, the job-finding rate is arguably one of the most important indicators to watch. This rate—defined as the fraction of unemployed workers in a given month who find jobs in the consecutive month—provides a good measure of how easy it is to find jobs in the economy. The chart below presents the job-finding rate starting from 1990. Clearly, the job-finding rate is still substantially below its pre-recession levels, suggesting that it is still difficult for the unemployed to find work. In this post, we explore the underlying reasons behind the low job-finding rate. According to the search and matching theory developed by Diamond, Mortensen, and Pissarides (see, for example, Pissarides [2000], Mortensen and Pissarides [1994], and Diamond [1982]), it is costly for workers and firms to form suitable matches because of the uncoordinated nature of the labor market. Workers must devote considerable time to sending out resumes, contacting job agencies, and interviewing for jobs, and firms must consume resources posting vacancies and recruiting candidates with suitable skills and talents. The process that matches workers to firms is typically summarized by a matching function, which determines the number of jobs formed given the number of vacancies and unemployed workers. According to the matching function, the main determinants of the job-finding rate are the ratio of job openings to the number of unemployed, (v/u), elasticity, α, and the matching efficiency, x: The vacancy-unemployment ratio summarizes demand and supply conditions in the labor market. When there are many job openings per unemployed individual, it is naturally easier to find jobs; conversely, it becomes harder to find jobs when there are many unemployed individuals competing for a small number of job openings. The parameter matching efficiency captures various factors that affect the efficiency of the matching process. An increase in skill or geographic mismatch, a decline in search effort of workers, or a decline in recruiting effort of employers would all lower the matching efficiency in the labor market. The elasticity, α, captures the responsiveness of the job-finding rate to the availability of jobs. As seen in the charts above, both the vacancy-to-unemployment ratio and matching efficiency declined during the Great Recession and have not recovered since. The matching efficiency is constructed under the assumption that the elasticity, α, was unchanged over this period. It is important to understand the contribution of each factor to the recent behavior of the job-finding rate, since the vacancy-to-unemployment ratio reflects labor market conditions, while matching efficiency is a measure of how well the labor market forms new matches. To isolate the contribution of these two factors, we regress the job-finding rate (unemployment-to-employment transition rate) on the vacancy-unemployment ratio using data until November 2007. The chart below shows that this regression captures the pre-recession behavior of the job-finding rate very well. We then use the relationship estimated using pre-recession data to generate predicted values for the job-finding rate starting in December 2007, as indicated by the bar. The predicted job-finding rate is an estimate of what the job-finding rate would be if matching efficiency had remained at its pre-recession level, but vacancies and unemployment had evolved as they did through the recession. As seen below, the actual job-finding rate currently lies below the predicted job-finding rate. However, one can also see that even the predicted job-finding rate still sits at 23.4 percent, significantly below its 2007 average of 27.8 percent. This implies that even if matching efficiency had returned to its pre-recession level and the economy had moved to the predicted line, the job-finding rate would still be significantly below its pre-recession levels. Our calculations suggest that while the efficiency of the U.S. labor market has not yet recovered, the most important factor is still the low vacancy-to-unemployment ratio. Finally, one can ask whether the observed decline in matching efficiency has been more or less pronounced in different sectors of the economy. The charts below examine this question for several representative industries, both in levels and using December 2007 normalized levels as the starting point. The plots show that matching efficiency has experienced declines across the board, with the possible exception of construction, where matching efficiency has returned to something close to December 2007 levels. We conclude that while matching efficiency has declined and remained low in virtually all industries, the most important factor in the low job-finding rate is the persistently low level of vacancies per unemployed. Disclaimer

|

| Why Trolls Start Flame Wars . . . Posted: 04 Mar 2014 04:30 PM PST Internet Psychology 101: Swearing and Name-Calling Shut Down the Ability to Think and Focus

Psychological studies show that swearing and name-calling in Internet discussions shut down our ability to think. Twi professors of science communication at the University of Wisconsin, Madison – Dominique Brossard and Dietram A. Scheufele – wrote in the New York Times last year:

So why do people troll in a rude way? Psychologists say that many Internet trolls are psychopaths, sadists and narcissists getting their jollies. It's easy to underestimate how many of these types of sickos are out there: There are millions of sociopaths in the U.S. alone. But intelligence agencies are also intentionally disrupting political discussion on the web, and ad hominen attacks, name-calling and divide-and-conquer tactics are all well-known, frequently-used disruption techniques. Now you know why … flame wars polarize thinking, and stop the ability to focus on the actual topic and facts under discussion. Indeed, this tactic is so effective that the same wiseguy may play both sides of the fight. Postscript: Fortunately, it's not that difficult to isolate the trolls and stop their disruption … if we just point out what they're doing. For example, I've found that posting something like this can be very effective:

Or this might be better if the troll is a sociopath:

(include the link so people can see what you're referring to.) The reason this is effective is that other readers will learn about the specific disruption tactic being used … in context, like seeing wildlife while holding a wildlife guide, so that one learns what it looks like "in the field". At the same time, you come across as humorous, light-hearted and smart … instead of heavy-handed or overly-intense. Try it … it works. |

| Posted: 04 Mar 2014 02:00 PM PST My afternoon train reading:

What are you reading?

|

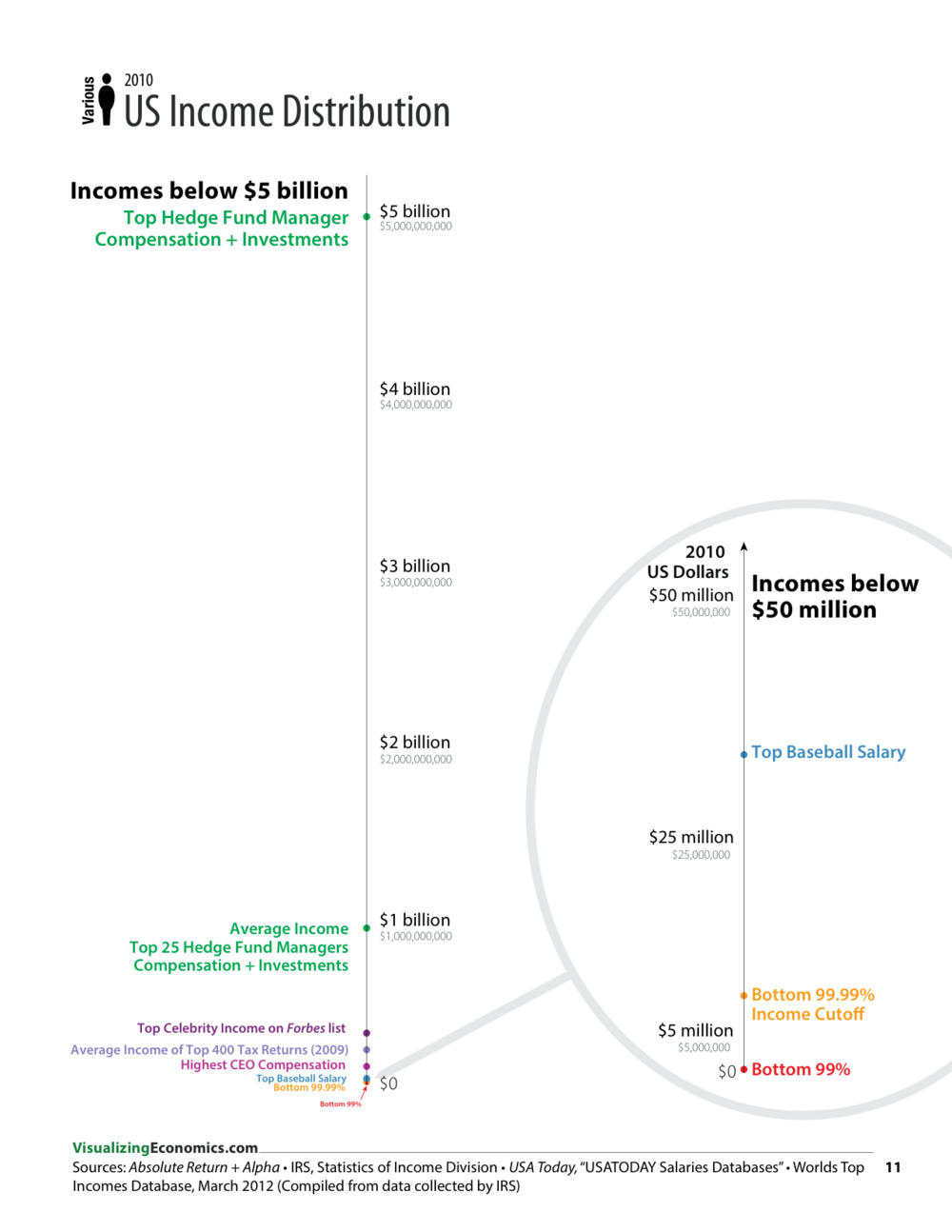

| Income Distribution Like You Have Never Seen It Posted: 04 Mar 2014 11:30 AM PST click for larger chart

When it comes to the top 0.01 percent of earners, it is extremely challenging to describe the differences in terms of income. Words often fail to convey the massive range. Fortunately for us, Catherine Mulbrandon of Visualizing Economics has put together a simple chart that shows just how fantastic the spread was in 2010 between those who are merely rich and the fabulously wealthy. This is an unweighted scale. It isn’t skewed for population. It merely ranks top incomes by dollars earned. |

| Mobile Usage Trends, Illustrated Posted: 04 Mar 2014 08:30 AM PST

|

| Posted: 04 Mar 2014 07:30 AM PST My morning reading, served fresh with corn muffins and coffee:

|

| The Putin Put: Ukraine Dragging Down Your Portfolio? Posted: 04 Mar 2014 05:30 AM PST On the first of each month, I send a letter to our investors describing what we see in the world relative to their portfolios. We always try to identify some "big picture" issue, usually one that is overlooked. The goal is to have our clients understand our thought process. One of my favorite analytical devices is to compare quantitative data with investor sentiment. Pitting the cognitive versus the quantitative often reveals a "perception gap" — a difference between investors' emotions versus the underlying market data. Think of it as "what people are thinking" versus reality. The news out of Eastern Europe is a perfect example of this. Russian President Vladimir Putin’s aggressive military grab in Ukraine has been dominating global media coverage. Markets were off dramatically yesterday, with Russian's bourse down 10 percent for the day. In the U.S., markets fell about 1 percent, although the accompanying media angst might have made you think it was triple that. Regardless, it is merely the latest global event that is dramatic, dangerous — and mostly irrelevant to investors. Why is that? |

| Posted: 04 Mar 2014 04:00 AM PST This is one of those things that really annoys me: One year ago today, Charles Nenner (of the Charles Nenner Research Center) went on TV. His specialty is Cycle Research (whatever that is). He made a very bold call, forecasting a drop to 5,000 in the Dow. It was not merely that the 50% drop did not come pass. What happened was the opposite, a 32% rally. And so, one year later, we have to recall this prognostication as one of the very worst of the year. The calls on Apple and Intel and Semis were nearly as bad.

Worst call of 2013: March 4 (Bloomberg) — Charles Nenner Research Center Executive Director Charles Nenner discusses the markets and his prediction of the Dow dropping to 5,000 this year.. He speaks on Bloomberg Television’s “Street Smart.” (Source: Bloomberg)

|

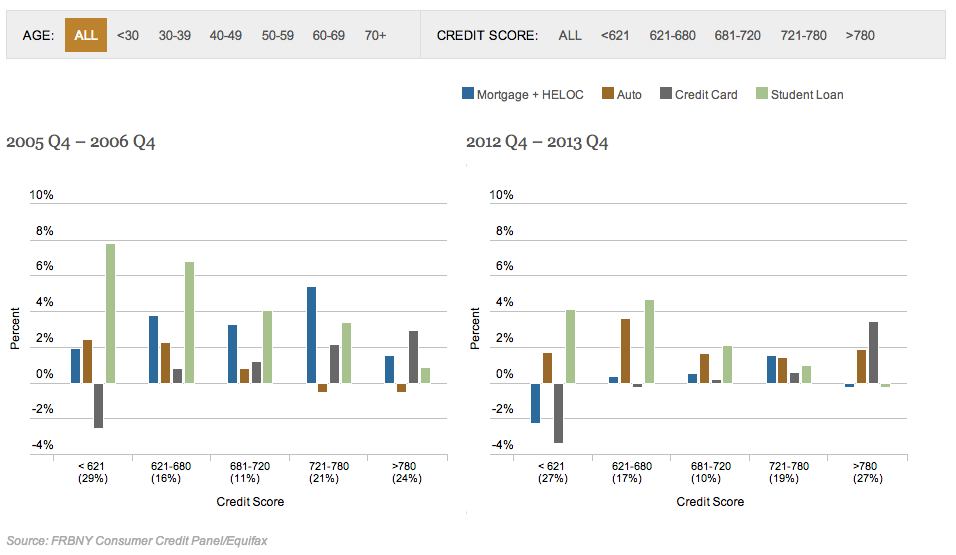

| Who’s Borrowing Now? Change in Debt by Credit Score and Age Group Posted: 04 Mar 2014 02:00 AM PST Click here for an interactive chart. |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment