The Big Picture |

- Peer-to-Peer Lending Is Poised to Grow

- Humanity’s Cultural History in 5-minutes

- Busy States of America

- Take It Easy: So Long, Summer 2014

- 10 Labor Day Reads

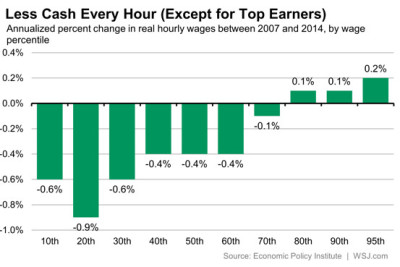

- Middle class households’ wealth fell 35 percent from 2005 to 2011

| Peer-to-Peer Lending Is Poised to Grow Posted: 02 Sep 2014 02:00 AM PDT Peer-to-Peer Lending Is Poised to GrowYuliya Demyanyk and Daniel Kolliner Peer-to-peer lending—a type of lending which matches individual borrowers with investors—is a recent innovation. But because it fills at least two gaps left by traditional lending sources, the peer-to-peer-lending market is likely to continue growing for some time. Emerging first in the United Kingdom in 2005 and arriving in the United States a year later, the peer-to-peer market has been growing rapidly since its inception, while traditional consumer bank loans and credit-card lending have been declining. Since the second quarter of 2007, the total amount of money lent through bank-originated consumer-finance loans has been declining on average 2 percent per quarter and the total amount lent through bank-originated credit cards has been declining on average 0.7 percent per quarter. Meanwhile peer-to-peer lending has been growing rapidly at an average pace of 84 percent a quarter.

Peer-to-peer's rapid growth may be attributable to two of the benefits it provides. First, it can improve access to credit for individuals who have short credit histories. Second, it allows consumers to consolidate credit card debt and lower their interest rate more than they could by going through traditional lenders. Peer-to-peer lenders use income, the type of employment, and even SAT scores in addition to credit scores and histories to assess the creditworthiness of borrowers. As a result, peer-to-peer lending could improve access to credit for consumers who, for example, are denied a loan by a bank because their credit histories are short, even if their credit scores are sufficiently high. A significant number of people fall into this category. According to data from Equifax, one of the three largest US credit bureaus, 39.8 percent of people with credit histories shorter than three years have credit scores higher than the subprime threshold, in other words, generally good enough to obtain a loan (Equifax, Federal Reserve Bank of New York’s Consumer Credit Panel). Most peer-to-peer loans are used to consolidate high-interest-rate credit card debt. Data provided by Lending Club, a company that arranges peer-to-peer loans, shows that 83.3 percent of peer-to-peer loans are personal one-time loans, most of which are put to use for this purpose. This may be explained by the fact that interest rates on peer-to-peer loans have been lower than those on credit cards since 2010:Q1.

Not every peer-to-peer borrower manages to obtain a better interest rate than a credit card rate. Peer-to-peer loans are categorized by grades A to D, reflecting the probability of default. On average, around 50 percent of loans are awarded a grade of "A" or "B." These consumers are considered the least risky borrowers, while borrowers with grades "C" or "D" tend to be riskier. Borrowers with loans graded "A" or "B" have consistently been getting better rates through peer-to-peer lending compared to credit cards. For borrowers with good scores, interest rates have a strong negative correlation with the credit card interest rates, meaning that when banks increase their interest rates, peer-to-peer lenders decrease theirs.

In comparison to bank-originated consumer-finance loans, peer-to-peer loans performed either similarly or slightly better. On average, between 2010:Q2 and 2014:Q1, 3.2 percent of peer-to-peer loans were past due compared to 3.7 percent of standard consumer finance loans. Over this period, peer-to-peer loans had a lower share of poorly performing loans in 10 of 16 quarters.

The peer-to-peer market is currently hundreds of times smaller than the consumer finance and credit card markets. However, the data suggest that the peer-to-peer lending market will continue to grow. One reason is that the supply of funds from investors for such lending has been increasing. Though peer-to-peer lending started as individual investors lending to individual borrowers, institutional investors, such as community banks, have become involved over time. Another reason that peer-to-peer lending is poised to grow further is that demand for such loans has been increasing. Individuals who either cannot get loans from traditional banks or who wish to consolidate their credit card balances at lower interest rates find peer-to-peer lending an attractive alternative. Source: Federal Reserve Bank of Cleveland |

| Humanity’s Cultural History in 5-minutes Posted: 01 Sep 2014 04:30 PM PDT From Nature:

Source: Nature |

| Posted: 01 Sep 2014 11:30 AM PDT |

| Take It Easy: So Long, Summer 2014 Posted: 01 Sep 2014 07:30 AM PDT The sun is out, the surf is up and it’s a beautiful Southern California day. That’s right, we might be plagued by earthquakes and gridlock, but when the elements align, which is nearly every day, when you get behind the wheel and crank up the radio, you feel like a million bucks. So I just went for an MRI at Kerlan-Jobe, for a hip injury that occurred skiing the ice two and a half years ago, I’m wondering what is causing the pain at this late date, and after lying in the tube for forty five minutes running every sexual fantasy possible through my brain to avoid concentrating on the fact that my ankles were Velcroed and my knee hurt I emerged into the sunlight to “Take It Easy” on the satellite. I’ve been thinking a lot about the last week of August. Used to be school was taboo. That week was taken up with recovering from summer exploits, before classes resumed after Labor Day. I’d come home from New Hampshire or Europe and immediately drive to Korvette’s to buy the latest albums, to catch up on what I missed when I was away. And that’s where and when I bought the Eagles’ debut. But it wasn’t only that, but Sly & the Family Stone’s “Fresh,” and a bunch of other records that I’d spin incessantly my first few weeks back at college in Vermont, where before you knew it, you were in the doldrums of November. But it’s different out here. The doldrums never appear. It rarely rains on your parade. And with no one asking where you went to college, never mind what you scored on your SATs, you’re free. And that’s what I love so much about SoCal, the right to be me, to live with a lawn and a car in a city where you may be unable to park, but at least you don’t feel closed in. So the world is blowing up, people’s rights are being challenged, opportunity is rare, yet when you emerge from your house into the SoCal sunniness you can’t help but smile and be optimistic. Never underestimate the weather. Yes, it’s weird how the days are getting shorter and the nights are getting colder. It’s like we’re beginning a four month run to Christmas, soon we’ll all be in front of the fire sipping hot cocoa. But not me! It’s the time of year when the Doors’ “Summer’s Almost Gone” goes through my brain. It’s the time of year when the boys of summer make their last pilgrimage to Malibu, before everybody hunkers down and gets serious. And it’s the time of year when “Maggie May” no longer resonates. Yup, for decades I was haunted by Rod Stewart’s refrain that it was late September and I really should be back in school. But no more! You see I’ve broken free. I am who I am, the story cannot be rewritten. And whether I’m happy with what’s inscribed in the book of life or not there’s nothing I can do about it other than put on my sunglasses, slide back the sunroof and turn up the radio. So, so long summer 2014. It was hotter than usual in my house without air conditioning but I won’t be worrying about it for long. So long hot summer nights where I could bask in sunlight ’til nearly nine. And so long to the pressure to find a song of the summer, to make the most of the few months off. Because in the modern world you’re never off, you’re on all the time, tethered to your devices, working to stay ahead of the man. But the truth is I’m on an endless vacation. I listened to Jan & Dean, I got the memo, I came out west to live the Beach Boys’ lifestyle and found out… THEY WERE RIGHT! ~~~ |

| Posted: 01 Sep 2014 04:15 AM PDT Enjoy your last day off before the new school year starts tomorrow. No worries, we have you covered with these Labor Day My themed morning reads:

What's up for unofficial last day of summer?

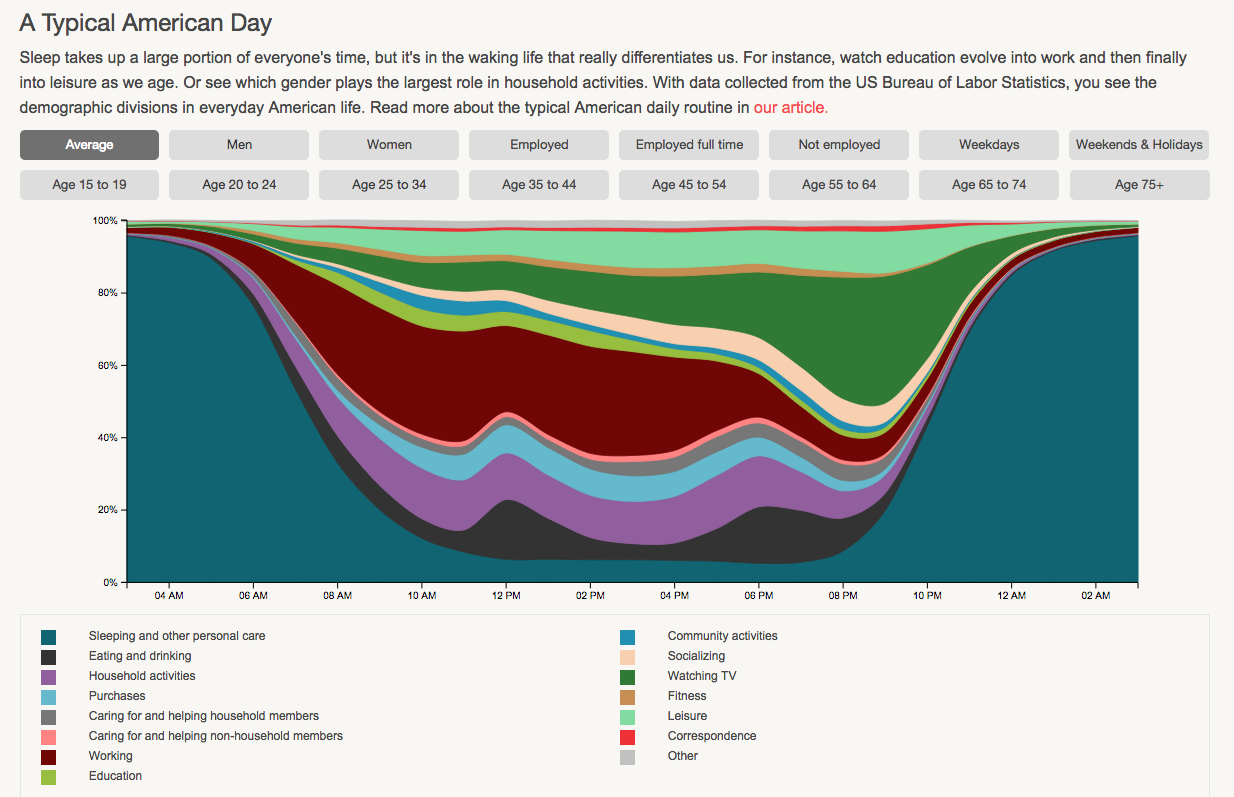

A Look at Income Inequality, Hour by Hour

|

| Middle class households’ wealth fell 35 percent from 2005 to 2011 Posted: 01 Sep 2014 03:00 AM PDT

|

/cdn2.vox-cdn.com/uploads/chorus_asset/file/666844/Screen_Shot_2014-08-22_at_2.15.58_PM.0.png)

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment