The Big Picture |

- Schizophrenic Financial Markets & Policy

- Big Banks Manipulated $21 Trillion Dollar Market for Credit Default Swaps

- Asness, Bogle on Investment Strategy, Pension Funds

- 10 Sunday AM Reads

- Kiron Sarkar’s Weekly Report 9.27.14

| Schizophrenic Financial Markets & Policy Posted: 29 Sep 2014 02:00 AM PDT Schizophrenic Financial Markets & Policy QUOTE # 1.

QUOTE # 2

QUOTE # 3

Thank you to Danny and Adam, John and Sarah, Ellen and Paula. You have set the stage for our discussion today and framed the debate for serious readers to consider. There is a debate in the US about the labor force, employment and wages. That debate takes place internally at the central bank, where contrasting views are regularly articulated by members of the Federal Open Market Committee (FOMC) as our Federal Reserve (Fed) policymakers attempt to steer monetary policy with regard to interest rates. Opinions and assertions about the condition of the US labor force are also offered by financial market participants, advisors, economists, and academics. The three papers cited above are part of that debate. They were written by skilled professionals who have identified, cited, and articulated views succinctly, eloquently, and usefully for anyone who takes the time to read them. I know some of the writers personally and I respect their work. The coincidence of all addressing labor force issues and income led to this weekend's commentary. In our view, the result of reading all three papers and others like them leads to a conclusion: we do not know the answers to the major problems the authors raise. We do not have certainty. We do have skilled opinions and assertions. Those of us in the financial market advising business are trying to grasp how labor force income will rise, at what rate, and in what cohorts, segments or components. We focus on different measures. The data are dependable. It is extensively assembled by means of systems that have been tested over many years. There is reliability in labor force data series. We are counting things well when we consider the margins for error. But interpretation and, hence, conclusions are difficult to come by. In fact, a large enigma remains unresolved, in that the labor force participation rate has been trending lower for a long time and has returned to levels last seen in the 1970s. At the same time, the unemployment rate may be inching upward. Were it to do so, it would signal that growing numbers of Americans seek a return to the labor force by declaring they have the confidence to find employment. If this phenomenon continued for several months – say, six data points – it would surely warrant a re-examination of many premises. We have yet to see that happen. Maybe an additional positive sign will appear with next Friday's monthly employment report. A positive report would read something like 250,000 new non-farm jobs, a slight tick up in the unemployment rate that is the result of a rising participation rate. That is a guess, not a forecast. We will look at the details carefully and the revisions. That is where we may be able to discern some trends. It would be good to observe sequentially rising income in the monthly employment reports. Higher pay levels broadly distributed among various categories of workers would indicate that income from labor is rising. It would mean that those who have to pay for labor are willing to pay more and those who provide labor (workers) are able to demand and obtain more. We have not seen that happen in a robust way. Where we do see it occur, it is isolated as opposed to broadly indicative. It would also be helpful if we saw the income inequality divide narrowing. That would say to us that the distribution of income (assumed also to be wealth, although that is not a perfect identity) is broadening. But as Ellen Zentner notes, income inequality in the US has been widening for decades. If the wealthy become wealthier, do they spend more on consumption? Are there levels at which "trickle down" ends in a drought? The answer is apparently a mixed but qualified yes. On the other hand, can we see some characteristics of the labor force that suggest that it is normalizing? The answer again is a qualified yes. One of my favorite statistics is pointed out by Jason Benderly, who suggests that households headed by a male adult with spouse present is a sector whose unemployment rate can be most consistently used to determine when wage pressure is beginning to rise. His reasoning is simple. If the head of household is a man, and it is an intact household in the traditional sense, that man is usually motivated to obtain income to support his family. Highly motivated workers are those who will find work and tighten the labor force more quickly. At some point that trend will be reflected in higher labor incomes. I also like to look at the single mom statistics, since single women who heads a household is part of a growing component of our society. Women who head households are a highly motivated cohort. In our labor force analytics, we observe both series. We see them improving. That says highly motivated heads of households, be they women or men, are seeking and obtaining jobs and gradually raising their incomes albeit at a slow pace. Will that trend lead to tightening conditions and then inflation pressure? We do not know. We have presented three papers that readers can view at their leisure in order to draw their own conclusions. The policymakers of the US central bank do not have the answers either. They have divided views, opinions, and assertions. Their current data is the same that we have. It goes without saying that the central bank is looking at history and attempting to drive policy forward. All of us know the peril of driving the car by looking in the rearview mirror. But in the present and confusing environment, history is all we have to help us. So what do we do with markets? Cumberland Advisors continues to modify duration in its managed bond accounts, either through hedging tactics or through shortening policies. We believe the short-term US interest rate will remain near zero for the rest of this year and well into 2015. Current market expectations suggest that the first Fed hike might occur in the summer of 2015. We are not sure. There may not be a hike for the entire year. Or the first tap on the interest-rate pedal may come earlier. As of this moment, there is no way to know. The result is schizophrenia in the discounting mechanism applied to short term interest rates. The bond market is schizophrenic, too. One day it forecasts higher interest rates, and bond investors panic. The next day, data suggest the opposite. Resulting bond market disarray ensues and rising bond interest rates seem way out in the future. The market rallies. Schizophrenia prevails in the bond market. The US stock market struggles with persistently very low interest rates and high liquidity. All of that is due to central bank policy. Meanwhile geopolitical risk rises; headline risk rises; and the new phenomenon of a structurally strengthening US dollar develops. Volatility in stock markets (VIX, SKEW) is reactive. Valuation metrics suggest the market is priced at a high level yet liquidity abounds and its influence is intense. Stocks, too, have schizophrenia. At Cumberland Advisors, we expect a long stretch of rising US dollar strength compared with most other currencies worldwide. Our portfolio shifts reflect that. We are also aware of the geopolitical risk that is abundant in the world and may precipitate a "black swan" event at any time. That could lead to a correction in stock prices. Stock, bond and liquidity market agents are evidencing schizophrenia. At Cumberland, we are maintaining some cash reserves in our exchange-traded fund portfolios as this is written. That cash could be redeployed at any time. ~~~ David R. Kotok, Chairman and Chief Investment Officer |

| Big Banks Manipulated $21 Trillion Dollar Market for Credit Default Swaps Posted: 28 Sep 2014 10:30 PM PDT

Derivatives Are ManipulatedRunaway derivatives – especially credit default swaps (CDS) – were one of the main causes of the 2008 financial crisis. Congress never fixed the problem, and actually made it worse. The big banks have long manipulated derivatives … a $1,200 Trillion Dollar market. Indeed, many trillions of dollars of derivatives are being manipulated in the exact same same way that interest rates are fixed (see below) … through gamed self-reporting. Reuters noted last week:

In other words, the big banks are continuing to fix prices for CDS in secret meetings … and have torpedoed the more open and transparent CDS exchanges that Congress mandated. As shown below, Wall Street has manipulated virtually every other market as well – both in the financial sector and the real economy – and broken virtually every law on the books. Interest Rates Are ManipulatedBloomberg reported in January:

To put the Libor interest rate scandal in perspective:

Currency Markets Are RiggedCurrency markets are massively rigged. And see this and this. Energy Prices ManipulatedThe U.S. Federal Energy Regulatory Commission says that JP Morgan has massively manipulated energy markets in California and the Midwest, obtaining tens of millions of dollars in overpayments from grid operators between September 2010 and June 2011. Pulitzer prize-winning reporter David Cay Johnston noted in May that Wall Street is trying to launch Enron 2.0. Oil Prices Are ManipulatedOil prices are manipulated as well. Gold and Silver Are ManipulatedGold and silver prices are "fixed" in the same way as interest rates and derivatives – in daily conference calls by the powers-that-be. Bloomberg reports:

Commodities Are ManipulatedThe big banks and government agencies have been conspiring to manipulate commodities prices for decades. The big banks are taking over important aspects of the physical economy, including uranium mining, petroleum products, aluminum, ownership and operation of airports, toll roads, ports, and electricity. And they are using these physical assets to massively manipulate commodities prices … scalping consumers of many billions of dollars each year. More from Matt Taibbi, FDL and Elizabeth Warren. Everything Can Be Manipulated through High-Frequency TradingTraders with high-tech computers can manipulate stocks, bonds, options, currencies and commodities. And see this. Manipulating Numerous Markets In Myriad WaysThe big banks and other giants manipulate numerous markets in myriad ways, for example:

The Big PictureThe experts say that big banks will keep manipulating markets unless and until their executives are thrown in jail for fraud. Why? Because the system is rigged to allow the big banks to commit continuous and massive fraud, and then to pay small fines as the "cost of doing business". As Nobel prize winning economist Joseph Stiglitz noted years ago:

Experts also say that we have to prosecute fraud or else the economy won't ever really stabilize. But the government is doing the exact opposite. Indeed, the Justice Department has announced it will go easy on big banks, and always settles prosecutions for pennies on the dollar (a form of stealth bailout. It is also arguably one of the main causes of the double dip in housing.) Indeed, the government doesn't even force the banks to admit any guilt as part of their settlements. Again Wall Street has manipulated virtually every other market as well – both in the financial sector and the real economy – and broken virtually every law on the books. And they will keep on doing so until the Department of Justice grows a pair. The criminality and blatant manipulation will grow and spread and metastasize – taking over and killing off more and more of the economy – until Wall Street executives are finally thrown in jail. It's that simple … |

| Asness, Bogle on Investment Strategy, Pension Funds Posted: 28 Sep 2014 03:00 PM PDT Clifford Asness, managing and founding principal of AQR Capital Management, and John C. Bogle, founder of Vanguard Group Inc., talk about investment strategy, fund management and the outlook for pension funds. Bloomberg’s Tom Keene moderates the discussion at the Bloomberg Markets Most Influential Summit in New York.

|

| Posted: 28 Sep 2014 05:00 AM PDT Pour yourself a cup of coffee, and sit back for some Sunday morning reads:

What’s for Brunch?

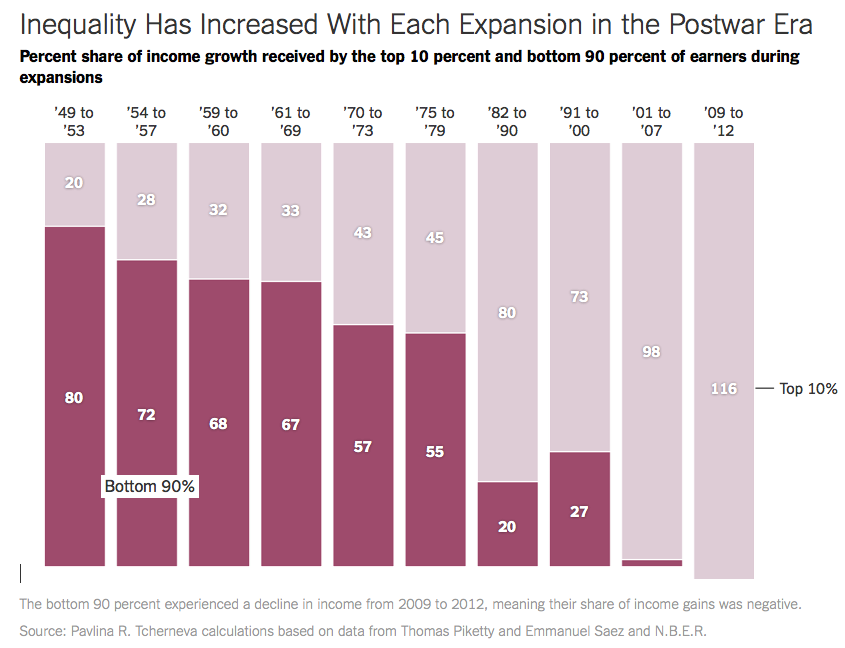

Inequality Has Increased With Each Expansion in the Postwar Era

|

| Kiron Sarkar’s Weekly Report 9.27.14 Posted: 28 Sep 2014 03:00 AM PDT The US, together with 5 Arab nations, launched air strikes against ISIS in Syria. Whilst positive that a number of Arab states are participating, this is going to be a long campaign. The Chinese finance minister, Mr Lou Jiwei, stated that growth faces downward pressure, though China will not make major policy changes to compensate. However, I suspect that at the end of the day the government will have to increase both monetary and fiscal stimulus, as the slowdown is far more severe than thought initially. The Wall Street Journal reports that the Chinese leadership is considering replacing Mr Zhou as head of the Central Bank in the next month or so. Mr Zhou has pressed for financial and economic reforms, rather than the interventionist policies pursued by the Chinese leadership. If he is to be replaced, the chances of further monetary and fiscal stimulus increases, which should help the commodities based currencies and equities. There are increasing signs that the Eurozone (EZ) economy is slowing. This has lead to speculation that the ECB will increase monetary accommodation. However, I suspect that the ECB will wait until its next TLTRO programme, together with its covered bonds/asset backed securities purchase programmes are launched before considering other options, which suggests no further changes this year. Next week’s inflation data will be important. Due to a further decline in energy prices and as a result of base effects, inflation may well fall further. With the exception of the US and the UK, the other major economies seem to be weakening. Emerging markets are also under pressure. The weaker global economy is reducing inflationary pressures, in particular due to lower commodity prices and a stronger US$. Lower inflation reduces the pressure on the FED to increase interest rates, though, for the present, I continue to believe that the FED will raise rates in H1 next year. The US 10 year bond yield declined to 2.50%, though the departure of Mr Bill Gross from Pimco, which bond investors believe will result in sales of US bonds by the firm as investor money follows Mr Gross to his new firm, resulted in yields closing at 2.53%. Global bond yields also declined. President Obama has suggested that he may reduce sanctions on Russia if it cooperates in enforcing the recent ceasefire in the Ukraine. There is speculation that Russia may introduce legislation to nationalise assets owned by foreigners. The situation remains uneasy to say the least. The US$ strength looks set to continue, whilst the Euro has weakened, a trend which I expect will continue. US The FED has warned banks that increasing the amount of high-risk assets on their balance sheets may well require them to hold additional capital. There have been a spate of "covenant-lite" high yield bonds issued this year, which Barclay's estimates will amount to over 70% of total issuances. In addition, total leverage on new deals has reached 4.95 times Ebitda, exceeding the highs reached in 2007. (Source Bloomberg). Capital goods orders (ex aircraft and defense) rose by +0.6% M/M in August, better than the increase of +0.2% in July and above the forecast for an increase of +0.4%. US weekly unemployment claims came in at 293k, better than the 296k expected, though above the previous weeks 281k. US Q2 GDP was revised higher to +4.6% on an annualised basis (the most since Q4 2011), in line with expectations and up from the previous estimate of +4.2%. Europe EZ September consumer confidence slipped to -11.4, from -10.0 in August and below the reading of -10.5 expected. The German IFO business climate index declined to 104.7 in September (the lowest since April 2013), down from 106.3 in August and below the forecast of 105.8. The current conditions component came in at 110.5, slightly better than the 110.2 expected, though below 111.1 in August, whilst the expectations component declined to 99.3, down from 101.2 expected and 101.7 in August. German flash manufacturing PMI declined to 50.3 in September, down from 51.4 in August and the forecast of 51.2. It was the weakest reading since June 2013. The new orders component declined to 48.8, from 51.1 previously, the 1st reading below the 50.0 neutral level since June 2013. However services PMI rose to 55.4, up from 54.9 in August. The composite PMI rose to 54.0, up from 53.7 in August. French flash September manufacturing PMI came in at 48.8, better than the 47.0 expected and above August's reading of 46.9. September flash services PMI came in at 49.4, lower than August's 50.3 and below the forecast of 50.1. EZ flash September manufacturing PMI came in at 50.5, slightly lower than 50.6 expected and August's 50.7. It was a 14 month low. EZ flash September services PMI declined to 52.8, slightly lower than the reading of 53.0 expected and down from 53.1 in August. The EZ flash September composite PMI declined to a 9 month low of 52.3, down slightly from 52.5 in August and below the forecast of 52.5. The decline suggests that the EZ economy slowed in Q3. The Spanish economy has improved materially over the last year. However, the Bank of Spain warns that private consumption and new job creation are weakening, which will result in Q3 growth slowing. However, the government has raised its 2015 GDP forecasts to +2.0% (+1.3% for 2014), from +1.8% previously. Japan CPI, excluding fresh food, rose by +3.1% Y/Y in August (+3.3% in July), below the rise of +3.2% expected. However, excluding the impact of the sales tax rise, CPI came in at just +1.1%, as opposed to +1.3% in July. Unless the Yen weakens materially, the BoJ is unlikely to meet its target of 2.0% target in the fiscal year beginning next April, which suggests that the BoJ will have to increase its monetary stimulus programme. Indeed, there is a risk that inflation will decline even further. China Chinese banks are likely to ease mortgage restrictions for 2nd home buyers, who will be eligible for a 30% reduction in mortgage rates. Yet another sign that the government is highly concerned about the property sector. Other A further sign of the weaker global economy is the decline in copper prices, which are at their lowest in more than 3 months. Clearly reduced demand from China is impacting. Crop prices have also declined and are near their lowest since 2010. The World bank reports that consumption in Russia, which is roughly 50% of the US$2 tr economy, will slow to +0.5% next year and +0.6% in 2016, down from +2.0% this year. They forecast that GDP will come in at +0.5% this year, lower than the +1.3% in 2013. GDP is forecast to reduce further to +0.3% in 2015 and +0.4% in 2016. Lower oil prices are also hurting the economy. The IMF warns that Saudi Arabia could face a budget deficit of -1.4% of GDP next year, significantly below its previous forecast for a surplus of +4.0%. Domestic expenditures have rocketed and the country has provided material aid to a number of other countries, a trend which is set to continue. Furthermore, the country is to increase infrastructure spending and welfare payments. S&P raised India's credit rating outlook to stable from negative, whilst maintaining its BBB- rating. The government has promised to reduce the budget deficit to 4.1% of GDP for the year ending 31st March 2015, down from 4.5% the previous fiscal year. That, I suspect, seems highly unlikely. Kiron Sarkar |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment