The Big Picture |

- Mr Abe’s comments cause a sell off

- Housing: Recovery … Or Artificial Bubble Which Is About to Pop?

- What Do You Do If You Miss the Move off of the Lows?

- 10 Midweek PM Reads

- Every Business Cliche Ever in One Toast

- Question: What Is Driving Hindenburg Omen Internals?

- 10 Midweek AM Reads

- Bureaucratic Blunder or Political Profiling at the IRS?

- Who Won the Iraq War?

- Early Withdrawals from Retirement Accounts During the Great Recession

| Mr Abe’s comments cause a sell off Posted: 06 Jun 2013 02:00 AM PDT Sarkar Global Macro is a newsletter which analyses and comments on market moving global macro issues, including an analysis of political and government policy decisions, which enables subscribers to make informed investment decisions. ~~~

Japanese PM, Mr Abe's speech on the country's growth strategy disappointed investors. He did not refer to restarting the country's nuclear programme, something a number of analysts had expected. He stated that he would promote private sector investment through the removal of bureaucratic barriers. He also promised to open up the infrastructure, health and energy sectors and promoting FDI into Japan, together with improving career opportunities for women. Certain cities would be allowed to introduce lower taxes and deregulate further creating, in effect special economic zones. Mr Abe also set a goal to increase earnings by 3.0%. All laudable sentiments, but there were few specifics or any meaningful measures and his statement will not make a difference in the short and medium term. The Nikkei reacted negatively with the market -3.8% lower and the Yen strengthening. Australasia Australia grew by just +2.5% in Q1 Y/Y, the slowest in nearly 2 years and below the +2.7% forecast. The lower growth, combined with the strong A$ and contained inflation, will add to speculation that the RBA will cut interest rates in the next few months. Analysts suggest that the RBA's benchmark interest rate will be cut to 2.0%, from the current 2.75%. The A$ clearly weakened on the news. As the EU has announced that it is to impose tariffs on chinese solar panels (see below), the Chinese have reacted by launching an investigation into the European wine sector. China is the fastest growing market for European wine and the 5th largest market globally. The speed of the retaliation has also caught EU officials by surprise, who had thought that the imposition of relatively low tariffs for a first few months would result in the Chinese seeking to negotiate a compromise. Chinese May services PMI rose to 51.2, from 51.1 previously. However, it was the lowest reading since August 2011. Chinese economic data just continue to slide and there are no signals that the new administration is prepared to stimulate the economy. I remain bearish on China. Indian authorities have increased curbs on the import of gold, which is a key driver of the current account deficit. Restrictions will be placed on banks and state run trading companies. The authorities are also tightening financing rules for imports. The measures have helped to stabilise (marginally) the Rupee, which was depreciating ahead of the announcement. India was the largest consumer of gold bullion last year, according to the Gold Council. Indian bond yields are drifting lower on speculation that the RBI will cut interest rates further, given the weaker economic growth. Europe EZ May final services PMI came in at 47.2, below the 47.5 expected, though above April's 47.0. Germany services PMI came in at 49.7, as opposed to 49.8 expected. France came in at 44.3, in line with expectations. Italy was weaker at 46.5, as opposed to 47.5 expected. However Spain was much better at 47.3, as opposed to 44.4 previously and expectations of 45.0. Once again, the PMI's are all in contraction territory, with Markit suggesting that the EZ economy will contract by -0.2% in Q2 The EU has imposed tariffs on solar panels imported from China. The rate of the levy is to be announced today, though will probably come in at a relatively low level and is expected to last for a few months, before increasing, and could be extended to 5 years. The EU in this way is trying to incentivise the Chinese to come to an agreement. The introduction of levies was opposed by a number of EU countries, including Germany, even though one of the main companies affected by this alleged dumping by Chinese manufacturers is a German company. The EU confirmed that Latvia's bid to join the Euro has been accepted and will happen with effect from the 1st January 2014. Whilst the EZ May services PMI came in weaker than expected, the UK services PMI came in at 54.9 (the highest since March 2012) and much better than the 52.9 in April and the 53.1 forecast. Markit, the provider of the data reported that the recovery appears to be gaining some traction, which was also evident in the recent manufacturing and construction PMI's. The data reduces the chances that the BoE will increase its QE programme. Other In a move to bolster its currency, the Brazilian authorities have cancelled the IOF (a financial transaction tax) of 6.0% on foreign investments in local fixed income markets, which was introduced in 2011 when its currency, the Real, was appreciating. The move is likely to help the Real in the short term, but I fear that Brazil's problems will resurface yet again. Trading volumes should increase, given the removal of the tax, adding to volatility. Markets Equities Australasia. Markets closed lower, with the Nikkei -3.8% weaker. Europe. European markets are lower and looking weak. US. Futures suggest a lower open. I remain cautious to negative. With uncertainty as to the FED's QE programme, the risks appear to be to the downside to me. Currencies Euro/US$ 1.3001 US$/Yen 99.53 £/US$1.5354 A$ 0.9557 The US$ is stronger against the Euro and the A$, but the Yen and £ are higher. Bonds 2/10 year Germany 0.11/1.53% Japan 0.12/0.85% UK 0.37/2.02% Relatively flat on the day. Commodities July Brent US$103.53 Gold is flat inspite of the news from India. Brent is creeping up again.

|

| Housing: Recovery … Or Artificial Bubble Which Is About to Pop? Posted: 05 Jun 2013 10:30 PM PDT Housing Prices: Up Or Down?

Preface: Part 1 will discuss what's really going on in the housing market. Part 2 explains why. CBS News noted in February:

The next month, CBS News reported:

Bloomberg point out:

[Indeed, mortgage applications are plunging.] Forbes wrote:

The Wall Street Journal noted:

In April, the Washington Post pointed out:

CNBC reported in May:

The New York Times explained Monday:

The Trend Is Not Necessarily Our TrendThe Wall Street Journal notes that investors are helping to speed the transition from a homeowner to a rental society:

Similarly, the Washington Post notes:

Will This End Badly?CBS News noted in February:

In March, the Wall Street Journal pointed out:

Yahoo's Daily Ticker asked:

In April, the Washington Post wrote:

Indeed, numerous institutional investors are starting to cash out. And there are reportedly mass layoffs coming in the mortgage finance industry. As the New York Times noted Monday:

|

| What Do You Do If You Miss the Move off of the Lows? Posted: 05 Jun 2013 05:00 PM PDT

I just submitted my Sunday column into be edited. The topic: You Missed the Big Market Rally? What Do You Do Now? I have my own ideas about what the best response is, but I wanted to open this up to the crowd: What should investors do when they miss a long rally? ~~~ What say ye?

|

| Posted: 05 Jun 2013 01:30 PM PDT My afternoon train reads:

What are you reading?

Sequester’s Bark Worse Than Bite—So Far |

| Every Business Cliche Ever in One Toast Posted: 05 Jun 2013 12:00 PM PDT |

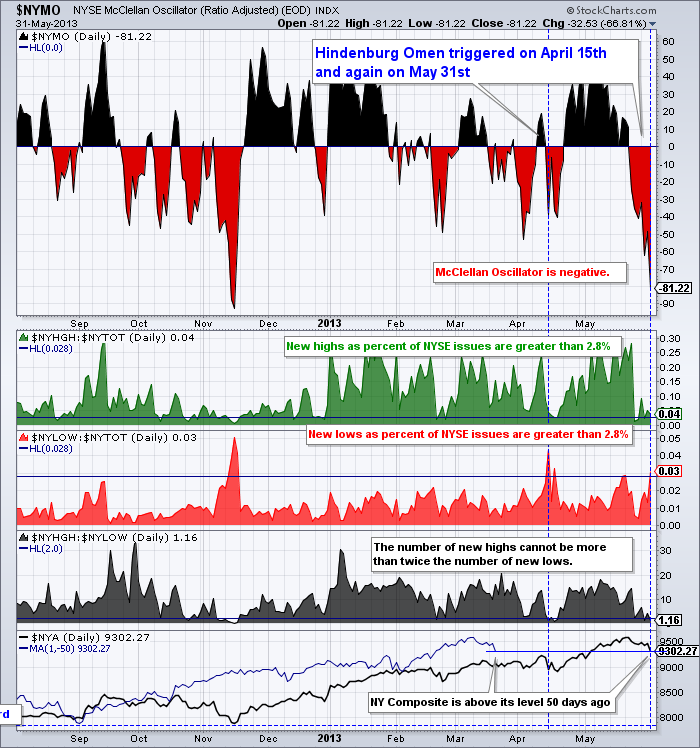

| Question: What Is Driving Hindenburg Omen Internals? Posted: 05 Jun 2013 10:00 AM PDT

Yesterday, we asked the question Why people fear the Hindenburg Omen? despite its mixed (i.e., awful) track record in forecasting crashes. Today, I have a more specific technical question: With markets up 16% YTD as of mid-May, we obviously had a huge number of stocks making 52 week highs. But we also have seen a spike in rates, suggesting that anything credit or bond related — closed end funds, mortgage REITs, bond funds, etc. — trading on the NYSE are going to be trading appreciably lower. Perhaps even to 52 week lows. Then there is Japan, and the large number of ADRs and ETFs on the NYSE. These may also be trading lower; the same for various European ADRs that are faltering. My technical question is this: What happens if we look at the NYSE US operating company only for this indicator — does it change its track record? Does removing the non equity names improve the signal’s otherwise mediocre track record? Alternatively, when successful Hindenburg Omens have been made in the past, are bonds/ADRs/closed end funds/non operating companies a factor? Is it possible to generate a track record using Nasdaq as the basis instead of the NYSE? What about the 500 names in the S&P500. Inquiring minds want to know!

|

| Posted: 05 Jun 2013 06:45 AM PDT My morning reads:

What are you reading?

Wall Street Takes Foot Off the Gas |

| Bureaucratic Blunder or Political Profiling at the IRS? Posted: 05 Jun 2013 04:30 AM PDT |

| Posted: 05 Jun 2013 03:00 AM PDT Iraq repays America by awarding oil contracts to China. Chinese Oil Drill (04:13) |

| Early Withdrawals from Retirement Accounts During the Great Recession Posted: 05 Jun 2013 02:00 AM PDT |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

1 comments:

Wow, this piece of writing is nice, my

sister is analyzing these things, thus I am going to let

know her.

Look at my web site билайн

Post a Comment